The Ultimate Year-End Bookkeeping Checklist

Year-end bookkeeping is a critical process that ensures accuracy, compliance, and readiness for tax filings and audits.

Whether you're a small business owner, accountant, or bookkeeper, following a structured year-end checklist can help you avoid common pitfalls and close the year on solid footing.

This blog will take you through the basics of bookkeeping, the details of year-end procedures, and how tools like QuickBooks and SaasAnt can optimize your workflow.

This guide is intended for bookkeepers, accountants, and small business owners seeking a structured, efficient, and accurate approach to year-end bookkeeping.

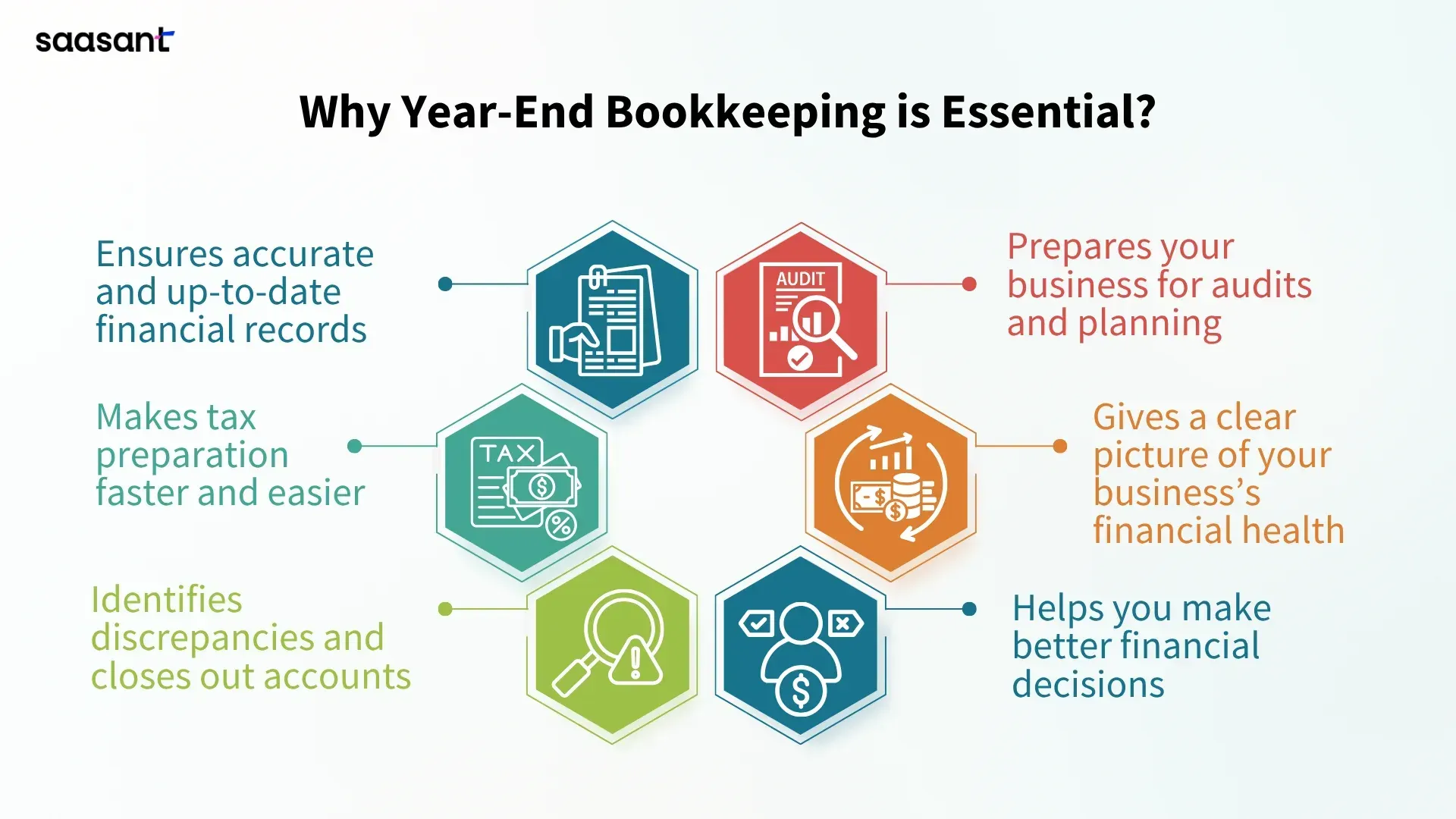

Year-end bookkeeping is essential for maintaining accurate records, ensuring tax readiness, and providing business clarity.

Key steps include organizing documents, reconciling accounts, recording transactions, and closing temporary accounts.

Reviewing payroll, inventory, and trial balance is crucial for identifying errors before year-end.

Backing up financial data is important for safeguarding information and preparing for tax deductions and filings.

Utilize tools like QuickBooks for automation and SaasAnt for efficient management of large financial data volumes.

Implementing a structured checklist can enhance business readiness for the new fiscal year.

Contents

What is Bookkeeping?

What is Year-End Bookkeeping?

Year-End Bookkeeping Checklist

Why Year-End Bookkeeping is Essential?

How QuickBooks and SaasAnt Make Year-End Bookkeeping Easier

Wrap Up

Frequently Asked Questions

What is Bookkeeping?

Bookkeeping is defined as the structured recording, organization, and tracking of a company's financial transactions. This includes maintaining accurate records for all income, expenses, assets, liabilities, and equity through the use of general ledgers, journals, and bank statements.

It ensures that businesses can evaluate their performance, comply with regulations, and prepare accurate reports.

Also Read: https://www.saasant.com/blog/bookkeeping-best-practices-for-ecommerce-businesses/

What is Year-End Bookkeeping?

Year-end bookkeeping, often referred to as "closing the books," refers to the process of reviewing, reconciling, and ensuring that all financial transactions and components of the company's ledgers from the last financial year are accurate. This includes calculating business expenses, income, revenue, assets, investments, equity, and other relevant financial metrics. The purpose is to create a final financial statement for a possible external audit, which will be kept within the company’s official financial records.

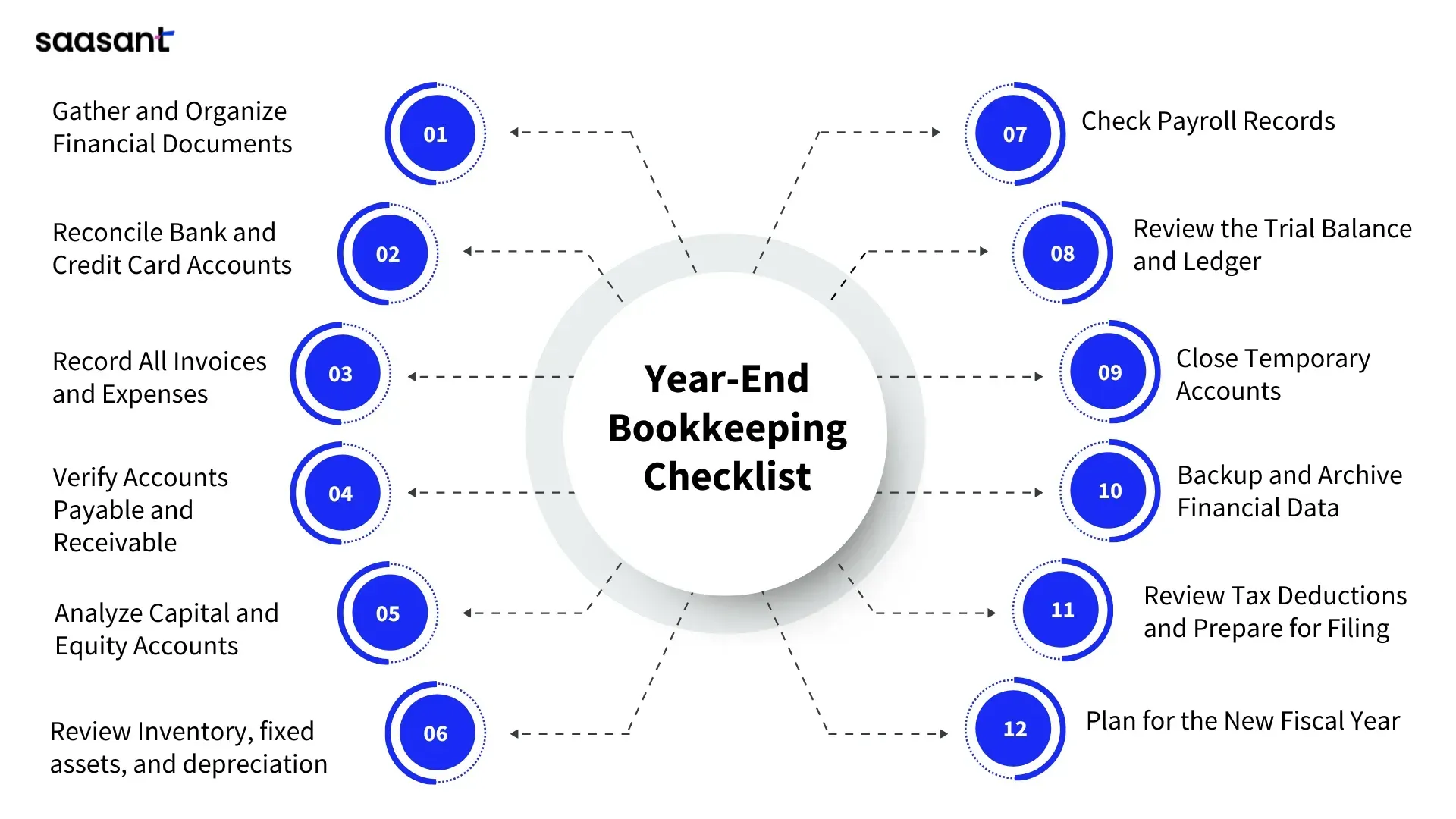

Year-End Bookkeeping Checklist

1) Gather and Organize Financial Documents

Compiling essential financial documents is a significant first step in the year-end bookkeeping process. This includes collecting bank and credit card statements, loan and merchant account statements, payroll reports, inventory counts, and last year's tax return. Maintaining these records in digital format ensures easy access, facilitates improved teamwork with your accountant, and promotes a smoother year-end closing process.

2) Reconcile Bank and Credit Card Accounts

Reconciliation plays a crucial role in identifying errors, fraud, or transactions that have not been properly recorded. It involves comparing bank statements with accounting records, addressing discrepancies, and settling outstanding checks or deposits that are more than six months old.

3) Record All Invoices and Expenses

Documenting all invoices and expenses is an essential part of a year-end bookkeeping checklist. This process involves collecting all invoices, receipts, and other relevant documents, and ensuring they are accurately entered into the accounting system with correct categorization and payment matching.

4) Verify Accounts Payable and Receivable

Reviewing accounts receivable and accounts payable is crucial for maintaining precise financial records. This includes verifying balances for customers and vendors, analyzing ageing reports, identifying overdue or uncollectible amounts, and reconciling sub-ledgers with the general ledger. Any required write-offs, adjustments, or accruals are documented to guarantee that the financial statements accurately represent actual liabilities and assets.

5) Analyze Capital and Equity Accounts

Evaluating capital and equity accounts is a crucial part of year-end bookkeeping, ensuring the accuracy of balances, reconciling transactions, and documenting any changes in ownership or equity. This process includes verifying balances, reviewing activities, analyzing equity changes, closing draw accounts, preparing entries, and examining financial statements. This process ensures the reliability of financial statements and informed decisions for the upcoming year, ensuring consistency and accuracy of financial data across accounting periods.

6) Review Inventory, fixed assets, and depreciation

At year-end, a careful review of inventory, fixed assets, and depreciation is paramount for accurate financial reporting. This involves conducting a thorough physical count of inventory, valuing it correctly at the lower of cost or market, and addressing any obsolete items. For fixed assets, it is essential to verify their existence, accurately document all additions and disposals, and evaluate for any impairment. Check the existence and condition of fixed assets, and log any additions or disposals. Ensure that depreciation schedules are updated and compliant. This process helps ensure accurate balance sheets, optimizes tax benefits, and maintains asset integrity for reliable year-end financial reports.

7) Check Payroll Records

The activity of auditing and confirming payroll records, which includes wages, bonuses, taxes withheld, and benefits. It highlights the significance of accurately classifying employees, verifying tax withholdings, benefits deductions, and contributions. This process also involves reconciling payroll information with tax submissions, verifying personnel classifications, and documenting any modifications or corrections made to the records.

8) Review the Trial Balance and Ledger

Reviewing the trial balance and general ledger ensures the accuracy and completeness of all financial data before the conclusion of the fiscal year. This process includes confirming that debits and credits are balanced, identifying any misclassifications or unusual entries, and making necessary corrections. Thoroughly reviewing each account helps to identify errors, omissions, or inconsistencies. A well-maintained, reconciled trial balance provides reliable financial statements and tax reports, helping your business maintain compliance and make informed decisions.

9) Close Temporary Accounts

Closing temporary accounts at the end of the year requires transferring balances from revenue, expense, and dividend accounts into retained earnings. This process resets these accounts to zero, setting them up for the upcoming fiscal year. It ensures that profit reporting is accurate and maintains an organized ledger.

10) Backup and Archive Financial Data

Backing up all financial data at the end of the year guarantees the safety and accuracy of your records. It safeguards against data loss due to system failures, unintentional deletions, or cyber threats. Storing backups securely on the cloud or external drives ensures data safety and supports compliance requirements. This step is essential before making final adjustments or closing the books.

11) Review Tax Deductions and Prepare for Filing

Analyzing tax deductions is a key aspect of year-end bookkeeping. Determine eligible business expenses like travel, utilities, and office supplies to maximize deductions and minimize taxable income. Ensure that all receipts and documentation are organized adequately for accurate reporting. This preparation simplifies the tax filing process and ensures compliance with tax laws. A proactive review also helps businesses plan their cash flow and avoid last-minute errors during filing.

12) Plan for the New Fiscal Year

Preparing for the upcoming fiscal year is a crucial aspect of year-end bookkeeping, which involves setting financial objectives, revising budgets, evaluating tax strategies, and ensuring that accounting practices align with business objectives. This strategy promotes a smooth transition, enhances financial preparedness, supports informed decision-making, streamlines processes, mitigates risk, and positions businesses for growth and compliance.

Also Read: https://www.saasant.com/blog/ecommerce-bookkeeping/

Why Year-End Bookkeeping is Essential?

How QuickBooks and SaasAnt Make Year-End Bookkeeping Easier

QuickBooks stands out as a premier accounting software, streamlining bookkeeping with features such as bank feeds, invoicing, and reconciliation. It automates routine tasks, such as bank reconciliations, payroll processing, and financial reporting. It helps you categorize expenses accurately and generate tax-ready statements with ease.

SaasAnt serves as a strong add-on for QuickBooks, designed to handle bulk data imports, exports, and automation. It integrates smoothly with QuickBooks, especially for e-commerce and payment gateway data.

Together, they reduce manual entry, minimize errors, and ensure your financial records are correct and ready for audits.

Also Read: https://www.saasant.com/blog/quickbooks-e-commerce-integrations/

Wrap Up

Year-end bookkeeping goes beyond just compliance; it’s a strategic process that sets the tone for the year ahead. Following a systematic checklist ensures that your records remain accurate, your tax preparation is simplified, and your business is well-prepared for future growth and development.

By leveraging trustworthy platforms like QuickBooks for your accounting processes and SaasAnt for transaction management and automation, you can enhance the overall workflow, minimize errors, save time, and acquire greater financial insight.

If you have inquiries regarding our products, features, trial, or pricing, or if you require a personalized demo, contact our team today. We are ready to assist you in discovering the ideal solution for your QuickBooks workflow.

Frequently Asked Questions

1) How early should I start preparing for year-end bookkeeping?

Preparation should ideally start at least 4-6 weeks before the end of your fiscal year. Early preparation provides the opportunity to sort records, reconcile accounts, and fix any discrepancies.

2) How does SaasAnt help with year-end bookkeeping?

With SaasAnt, you can import, export, and perform bulk edits on transactions, making it especially advantageous for handling extensive data volumes. It integrates seamlessly with QuickBooks to facilitate year-end procedures.

Read Also

Bookkeeping Best Practices For Ecommerce Businesses: Mistakes and Hidden Costs

A Clear Monthly Bookkeeping Workflow Checklist

Contractor Bookkeeping Made Easy with QuickBooks

Bookkeeping for Truck Drivers: Simplifying Your Finances with QuickBooks