Understanding Cash Flow Statement and Its Accounting Methods

A company's financial statement provides investors and analysts with an understanding of the transactions carried out and how each transaction contributes to the company’s success. The cash flow statement is crucial for creating a company's financial statements. Along with the balance sheet and income statement, cash flow statements provide a comprehensive picture of the company's overall economic performance.

This blog will walk you through direct vs. indirect cash flow statements, types of cash flow statements, what direct and indirect cash flow are, their examples, and how to choose the best cash flow method.

Contents

What is a Cash Flow Statement?

What are the Components of a Cash Flow Statement?

What is the Utility of a Cash Flow Statement in a Business?

What are the Types of Cash Flow Statements?

What is Direct Cash Flow?

How is Direct Cash Flow an Accounting Method?

What is Indirect Cash Flow?

Direct vs. Indirect Cash Flow

How to Choose the Best Cash Flow Method

FAQs

What is a Cash Flow Statement?

A cash flow statement includes all the cash inflows the company gains from its current operations and externally invested sources. Additionally, it contains cash outflows to be spent on business operations during the quarter. Accrual and cash accounting methods determine how a company's cash flow statement is represented. Cash flow statements, direct or indirect, give essential indications to the business by calculating various operating and sales ratios, free cash flows, and comprehensive cash flow coverage.

The critical fact about cash flow in business is that it is entirely different from earnings. Earnings indicate sales and expenses made in the present, while cash flow means cash inflows and outflows that occur later.

What are the Components of a Cash Flow Statement?

A cash flow statement is divided into three sections: cash flow from operations, investing, and financing activities. Let’s look into it in detail:

Cash flows from operations:

The first section of the cash flow statement is cash flow from operations. This section records all inflows and outflows resulting from operational activities. In other words, cash flows from operations is a company's net income in a cash version. This section includes all the income and expenses from the company's direct operating and business activities. All these business activities include buying and selling inventory and supplies. It also includes paying salaries to their employees. Generally, companies usually earn enough inflows from their operating growth.

However, the companies resort to investments and financing if they need additional cash flow. A company calculates its cash inflows and outflows based on operating activities, including revenue generated, expenses paid, and funding working capital. It is calculated by considering the company's net income, adjusting the non-cash items, and changing the working capital.

Managing all the above-mentioned operating activities becomes easier when using accounting software like QuickBooks to manage your finances. To handle all your transactions in QuickBooks, you can use an automation tool like SaasAnt Transactions. It helps you with the automation process and ensures accuracy and workflow efficiency.

The exact formula for calculating cash flow from operating activities may differ from company to company-based income statements and balance sheets. However, a generic formula to calculate the cash flow from operating activities can be mentioned below:

Cash flow from operating activities = Net Income+ Non-Cash Items+ Changes in working capital.

A few examples that go under operating cash flows include cash received from sales, changes in current assets/liabilities that are due in a year or less, accounts payable, depreciation, amortization, various prepaid items booked under revenue or expenses, salaries paid out to employees, payments to vendors and suppliers, income from interests and dividends, income tax and its interest, etc.

Cash flows from investing:

It is the second most crucial element of a cash flow statement, which records cash inflow and outflow from purchasing and selling assets, properties, equipment, etc. All inflow and outflow based on assets and investments are a part of this section.

Cash flow from investing activities provides insight into future cash inflows and long-term value.

It is utilized by investors and business analysts to assess planned capital expenditures.

The investment activities section on the cash flow statement is crucial for understanding current and future capital and growth prospects.

Capital expenditure signals investment in future growth, indicating significant growth potential.

A strong focus on operating activities in cash flow is essential for indicating solid fundamental business growth.

The investing section of the cash flow statement gives investors a clear view of the company's self-investment levels.

Examples of cash inflows and outflows from investing activities are the purchase or sale of a fixed asset, the purchase or sale of investment in stocks and securities, lending money, the collection of loans and insurance, etc.

Cash flow from Financing Activities:

Cash flow from financing is the last section of the company's cash flow statement that gives an idea of the company's capital raising and financing activities. It is usually a picture of a company's debt and equity activity, and it measures the cash flow between the company, its owners, and creditors. These figures are generally reported on an annual basis.

Analysts and investors take help from this section to determine how much money has been paid in the form of buybacks or dividends and how the company raises finances for its operational growth. The company's cash flow from financing activities indicates the general cash inflows and outflows in the business that are used to fund the company and its fundamental activities. This section also provides the investors insight into the strength of the company's finances and how well it manages its capital structure.

If a business is sound on its financial footing, investors and analysts use the following formula to determine the company's cash flows from financing activities:

Formula:

Cash flow from Financing Activities: Cash inflows from issuing equity or debt - (Cash paid as dividends + Repurchase of debt or equity)

Cash flow from the financing activities includes transactions that involve debt, equity, and dividends.

What is the Utility of a Cash Flow Statement in a Business?

Whether it is the business owner, an investor, or an analyst, knowing how to read all company statements is vital to getting a clear picture of the financial abilities of the company. Cash flow statements are essential to any business because various stakeholders are involved in a company's well-being.

Cash flow statements are essential for a business person because they help you understand the company's current position and make critical adjustments and strategic changes. As an investor, cash flow statements give a clear picture of the company's financial stability and insight into the company's future growth prospects. It is essential because it demonstrates the organization's ability to operate in the short and long term based on how much cash flows into the system.

What are the Types of Cash Flow Statements?

Direct and indirect are the two different methods used to prepare companies' cash flow statements.

In the direct cash flow case, changes in the cash receipts and payments are reported in cash flows from the operating activities section.

On the contrary, in the indirect cash flow method, asset and liability account changes are adjusted in the net income to arrive at cash flows from the operating activities.

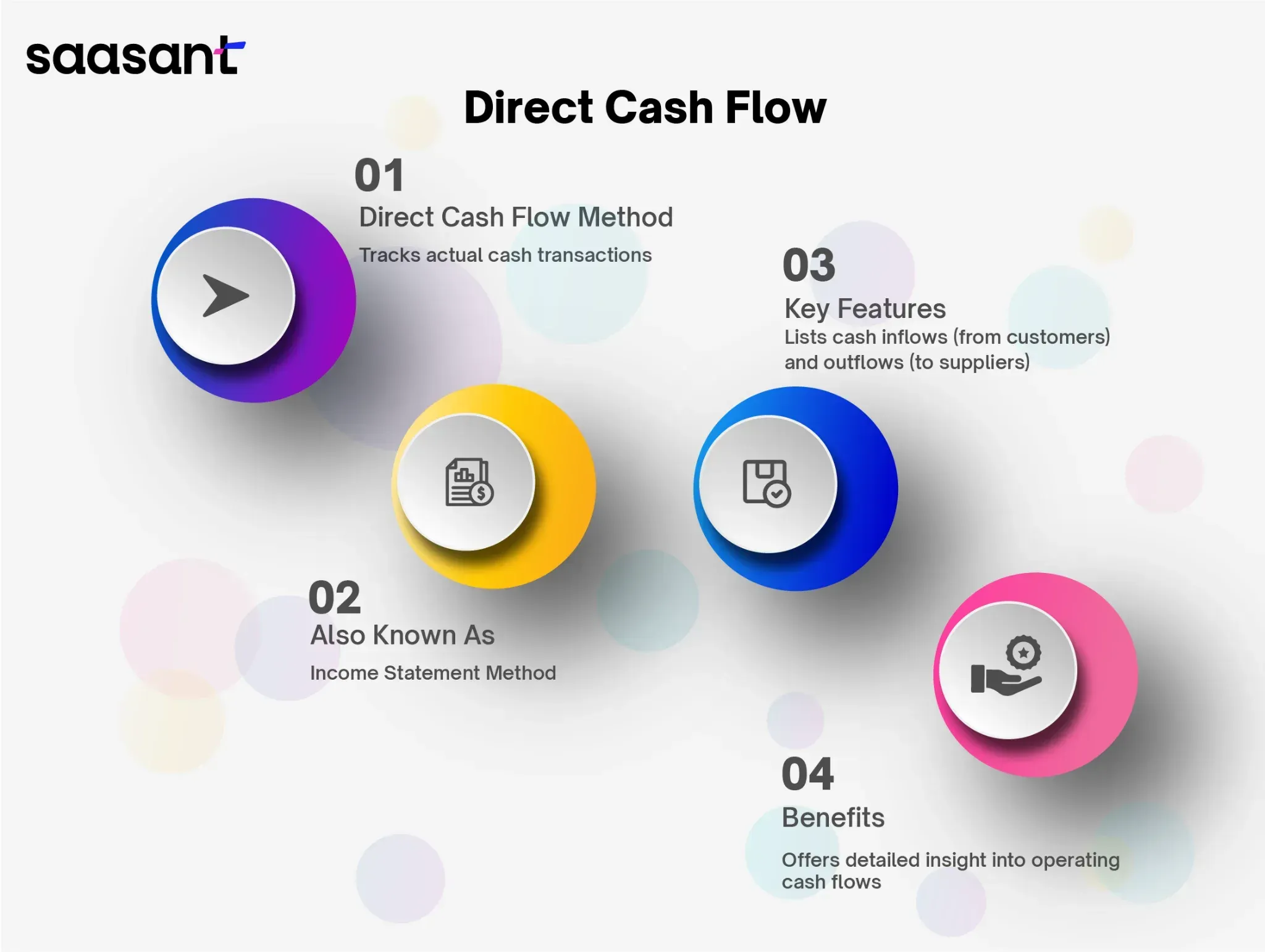

What is Direct Cash Flow?

A direct cash flow method generates detailed sources of a company's cash inflows and outflows/reason for cash outflows. It considers the actual cash inflows and outflows instead of modifying the accrual accounting on a later basis. Unlike accrual accounting, this method only measures the cash received, typically from customers, and cash payments or outflows, such as payments made to suppliers. The direct cash flow method is called “the Income Statement Method.”

The cash flow statement made through the direct method determines changes in cash receipts and payments reported from the operations section. Although the direct method is time-consuming, it gives a more detailed outlay of the operating cash flows in the business. The direct method of cash flow statement lists cash outflows and inflows to calculate the net cash flow from operating activities. After that, the net cash from investing and financing activities is included to increase or decrease the company's net cash.

Example of a Direct Cash Flow Statement

Salaries paid to employees

Cash paid to vendors/suppliers

Cash collected from customers

Interest income and dividends received, etc.,

How is Direct Cash Flow an Accounting Method?

The direct statement of cash flow provides a clear picture to investors and analysts, allowing them to predict future cash flows and earning potential. This worldwide accounting method encourages direct cash flow statements because of their transparency.

Various businesses are heavily transactional and have many cash inflows and outflows daily. Recording daily transactions using the direct cash flow method becomes very time-consuming for such businesses.

Additionally, this work is labor intensive and adds to the business' cost.

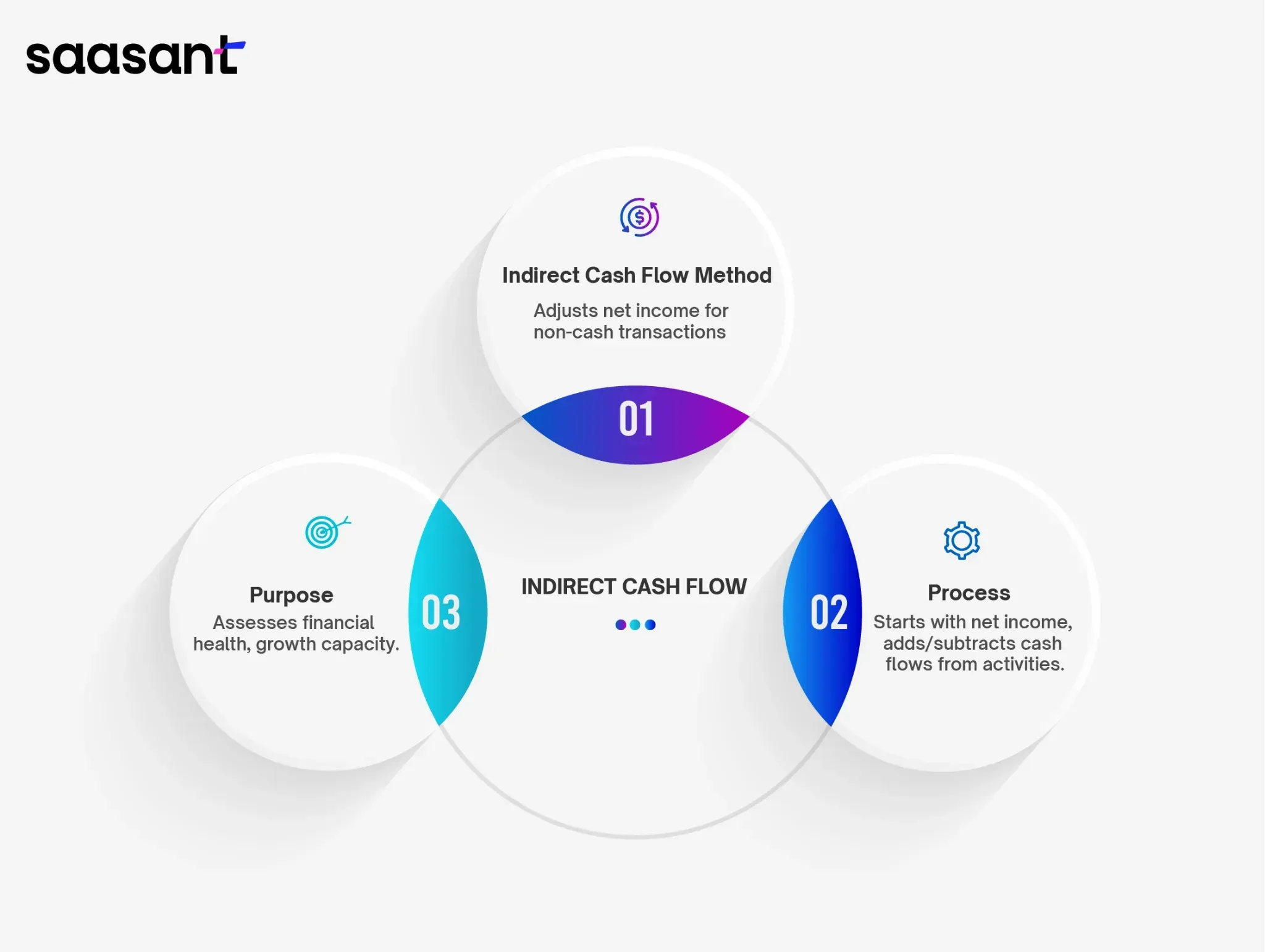

What is Indirect Cash Flow?

The indirect cash flow method is a way to calculate cash flow using transactions to determine payments and expenses rather than cash on hand. It measures how much a company makes or spends. It helps evaluate a business's current or relative health and financial stability and whether it has money to spend on growth and other investments.

The indirect cash flow method calculates cash flow by adjusting net income with differences from non-cash transactions. It starts with a business's net income and then lists cash flows, received and paid, for various activities. These activities are then added or subtracted from the business's net income to determine its final net cash increase or decrease over the specified period.

Example of an Indirect Cash Flow Statement

When understanding the concept of direct vs. indirect cash flow statements, an example or, more precisely, some examples of Indirect cash flow statements can include expenses like depreciation, cash flow from financing activities, proceeds from the issue of common stock, etc.

The indirect method is easy to use and a less time-consuming process. It becomes a cost-effective method for businesses as each cash transaction does not need to be involved. The indirect method gives summarized data on the cash stability of the company, including its future growth aspects.

Tracking each cash inflow or outflow can be very time-consuming and challenging. It gives a snapshot because the indirect method often calculates and maintains cash flow quarterly or yearly. It may need help to get a clear picture of the business's stability.

Direct vs. Indirect Cash Flow

Direct cash flow tracks variations in actual cash receipts and disbursements as reflected in the cash flow statement. Indirect cash flow starts with net income and adjusts for non-cash transaction changes to estimate cash flow. Let’s understand the difference between indirect vs direct cash flow:

Direct Cash Flow | Indirect Cash Flow | |

Explanation | The direct method employs actual transaction data, focusing exclusively on cash movements to display tangible receipts and disbursements. | The indirect method modifies net income by accounting for adjustments stemming from non-cash activities. |

Make use of preference | Not commonly used by accountants, this method best suits small businesses with minimal cash transactions. | Widely adopted by publicly traded companies undergoing routine audits, this approach leverages data from income statements and balance sheets for swift accuracy verification. |

Accuracy | Straightforward in concept, yet typically more intricate in computation. | Conveniently computed from a company’s general ledger and accrual accounting system. |

Effort and Time | May not satisfy the accounting needs of specific organizations due to the need for a comprehensive list of all cash transactions, necessitating significant time and effort. | Generally simpler and less time-consuming to compile, as most organizations maintain their records on an accrual basis, reducing the effort required. |

How to Choose the Best Cash Flow Method

There are various questions to ask before choosing the best reporting method: What is the desired reporting workflow? What are the reports being created for? How detailed does the report need to be? A smaller business that looks for clarity in finance may use the indirect method, while the indirect method is used for reports that only need comparative data. A direct method is convenient if the reports are made for investors, banks, analysts, or prospective clients. However, if the reports are made for internal processes, any more accessible and transparent method for the business shall be considered.

Depending on the depth of reporting you're looking for, you can commit the work to a direct reporting method. While compiling takes longer, the direct method gives a more transparent view of your cash inflows and outflows. One method will make more sense once you've considered what you're trying to do with your cash flow statement.

FAQs

What are the advantages of a direct method cash flow statement?

A company's cash flow statement reflects its financial performance over a specific period. The direct method is especially beneficial for smaller companies with fewer fixed assets since it relies solely on actual cash transactions to determine total earnings and expenditures.

Why is the indirect method of cash flow better?

The indirect cash flow method is better as financial statements are more accurate. The indirect method arrives at the net operating cash flow figure by starting with the calculated net income and adjusting for non-cash items. This introduces a more significant potential for mistakes and duplications.

Which method of cash flow is preferred?

Many accountants prefer the indirect method due to its simplicity in preparing the cash flow statement with data from the income statement and balance sheet. Since most companies focus on the accrual accounting approach, the income statement and balance sheet figures align with this methodology, making the indirect method more straightforward.

What is the difference between direct and indirect cash flow?

Direct cash flow analyzes variations in cash inflows and outflows as documented in a cash flow statement. On the other hand, indirect cash flow starts with net income and adjusts for non-cash transactions to estimate the actual cash flow.

What is the difference between direct and indirect cash flow CFA?

The indirect approach starts by taking the net income from the income statement and then includes non-cash items to determine a cash-based amount. On the other hand, the direct method records every transaction in a period based on cash and presents the actual cash inflows and outflows on the cash flow statement.

What is the difference between direct and indirect methods of cash flow PDF?

The direct cash flow method displays real cash transactions such as customer receipts and supplier payments. In contrast, the indirect method begins with net profit and accounts for non-cash items like depreciation.