Bookkeeping Best Practices For Ecommerce Businesses: Mistakes and Hidden Costs

According to Statista, the eCommerce market is projected to reach a staggering US$4.11tn in revenue by the year 2023. This is no small feat, as it represents a tremendous growth rate of 11.51% annually, resulting in a projected market volume of US$6.35tn by the year 2027.

Out of all the countries in the world, China is expected to generate the most revenue in the eCommerce market, with a projected market volume of US$1,487.00bn in 2023. This comes as no surprise, considering China's robust economy and large population.

The eCommerce market is also expected to see an explosion in the number of users, with a projected amount of 5.29 billion users by 2027. This marks a significant increase in user penetration, which is expected to hit 57.2% in 2023 and eventually reach 66.6% by 2027.

As more and more users flock to the eCommerce market, the average revenue per user (ARPU) is expected to rise as well, with a projected amount of US$930. These figures showcase just how lucrative the eCommerce market can be for those who are able to tap into it successfully.

The eCommerce market's expected growth, as projected by Statista, presents a wealth of opportunities for businesses to capitalize on this burgeoning industry. However, as eCommerce businesses look to maximize their revenue, it is essential that they establish sound bookkeeping practices to avoid costly mistakes and hidden expenses.

With so many transactions taking place in the online space, it is easy for businesses to lose track of expenses, overlook potential deductions, and ultimately end up with higher taxes owed. Moreover, chargebacks can also be a significant drain on revenue, causing businesses to lose not only the disputed transaction amount but also incurring chargeback fees from payment processors.

To ensure long-term profitability and success, eCommerce businesses must take proactive steps to establish bookkeeping best practices that not only keep them in compliance with regulatory requirements but also help them to identify cost-saving opportunities and reduce their financial risks.

Having seen firsthand the cost attached to poor ecommerce bookkeeping practices, we will first explore some of the best practices for bookkeeping in ecommerce businesses, and then highlight some common mistakes and hidden costs that online merchants often overlook.

Contents

Bookkeeping for Ecommerce business

What is the basic rule of bookkeeping?

What are best practices in bookkeeping?

Ecommerce Bookkeeping Mistakes and Hidden Costs (Implications) for your Business

Conclusion

FAQs

Bookkeeping for Ecommerce business

Bookkeeping is the process of recording financial transactions and maintaining accurate and up-to-date financial records. As an eCommerce business, your bookkeeping is crucial to keep track of sales, expenses, inventory, and cash flow.

The first thing to do in eCommerce bookkeeping is to create a chart of accounts. This is a list of all the accounts used to record financial transactions, such as sales revenue, cost of goods sold, advertising expenses, and shipping expenses.

Then, track your sales and expenses. This includes recording all sales transactions, such as orders placed through the eCommerce website, as well as all expenses incurred in running the business, such as marketing expenses, shipping costs, and software subscriptions.

If you run an inventory-based eCommerce business, then you need to track inventory levels and the cost of goods sold, as well as any adjustments made to inventory due to damaged or lost items. You also need to monitor your cash flow closely, that is, track incoming and outgoing payments, manage accounts receivable and accounts payable, and reconcile bank statements.

Finally, it's essential you regularly review financial statements, such as income statements and balance sheets, to assess the financial health of your business and make informed decisions about future investments and growth strategies.

What is the basic rule of bookkeeping?

The basic rule of bookkeeping is to maintain accurate and complete records of all financial transactions using the double-entry accounting system. The fundamental principle of double-entry bookkeeping is that for every debit, there must be a corresponding credit, and vice versa.

This ensures that the accounting equation is always balanced, where assets = liabilities + equity. An extension of this rule is that you should have supporting documentation, such as receipts, invoices, and bank statements to substantiate the recorded transactions.

What are best practices in bookkeeping?

“Business Owners should pay attention and check on the best practices for having a smooth bookkeeping workflow”

Regina Alpez Accountant-Consultant

In every industry, there are sets of guidelines or standards that produce good outcomes when followed. This is especially true for the bookkeeping and accounting industry with more than one basic rule guiding it. Since ecommerce is one of the fastest growing industries, many business owners lose track of the best practices and focus more on making more revenue.

To become a successful online business owner, you should take note of the following best practices.

Separate personal and business finances

Keep accurate record

Track your inventory

Reconcile your accounts regularly

Monitor your cash flow

Be updated on Tax Laws

Keep relevant documentation

Review all financial reports regularly to know your business performance.

Ecommerce Bookkeeping Mistakes and Hidden Costs (Implications) for your Business

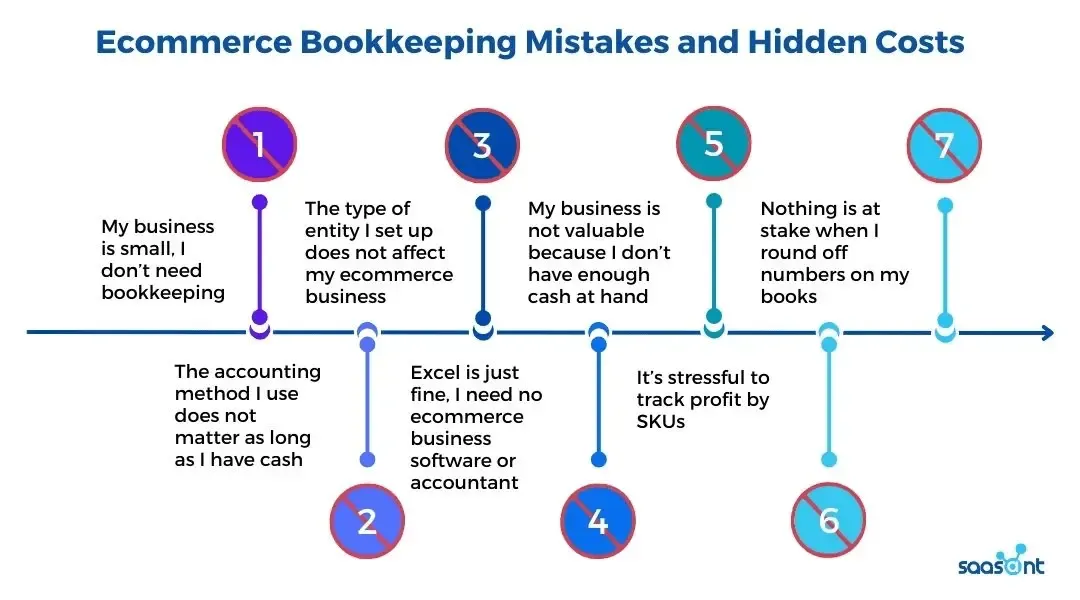

Neglecting bookkeeping practices comes with many negative consequences. Let’s dive into some of the common bookkeeping mistakes made by ecommerce business owners and the hidden costs (implications) it has on your business if you go that route. You will also find some small business bookkeeping tips as you read on.

#1 My business is small, I don’t need bookkeeping

Whether big or small, business owners should keep track of their financial progress to know profitability, sustainability and how fast their business is growing. With little or no bookkeeping, taking business decisions is like a blind man trying to cross the highway or drive a manual vehicle. You know the result already.

Without accurate record keeping, you cannot tell which part of your business is doing well or not. For example, to make informed decisions about what is chopping into your profit or which widget brings in most sales cannot be determined without proper bookkeeping.

How do you know you performed better than last month or year and which area to focus on for more growth? How do you obtain finance from investors and lenders without financial statements to show your business health. Never downplay bookkeeping because it has far reaching consequences on ecommerce business when done poorly.

#2 The accounting method I use does not matter as long as I have cash

You may be fortunate to have proper bookkeeping but don’t care about the accounting method you used, whether cash or accrual accounting. Cash accounting is the easiest to monitor and many business owners practice it.

In cash accounting, when you buy a widget, you record the expense when you pay and recognise revenue when it is received. The implication of this method is that you can conclude business is doing well when you receive more cash (during sales) and vice versa when less cash comes in or when you have to purchase large inventory.

This method does not help you to really know how your business is doing. On the other hand, accrual accounting looks at every activity and not just cash received or paid. In this case, the inventory sold (even though cash has not been received) is recognised as earned revenue.

Similarly, when you purchase a large inventory and the cash is yet to be deducted from your bank account, it is recognised as an expense already. Let’s look at an example to cover both scenarios.

If Shopify deposits $100,000 as your July sales and ecommerce platform charge is $20,000, but will be deducted in August. Accrual accounting method recognizes both the Expense and the Revenue in July and deposits $80,000, whereas cash accounting records $100,000 in January and waits till February before deducting the $20,000.

Whereas cash accounting makes it hard to really know your true condition, accrual method lines up sales, COGS (Cost Of Goods Sold), platform fees and expenses on a monthly basis.

Concerning taxes, whichever method you use to do bookkeeping does not dictate the method you use to file your taxes. So, if you choose accrual over cash, you are not under any obligation to choose the same method for filing taxes.

Tip: Most CPAs believe you save money by filing taxes on a cash basis.

#3 The type of entity I set up does not affect my ecommerce business

Unfortunately, it does! The type of entity has a direct impact on your ecommerce taxes. Sometimes you are in haste to take advantage of a business opportunity that you forget to set it up as efficiently as you should.

Both S Corporations (S Corp) and Limited Liability Companies (LLCs) are popular business structures that offer liability protection for owners. However, they differ in terms of taxation and distribution of profits.

Self-Employment Tax:

LLCs are typically subject to self-employment tax, which includes both the employer and employee portion of Social Security and Medicare taxes. The entire net income of the LLC is subject to this tax, regardless of whether it is distributed to the owners or retained in the business.

On the other hand, S Corporations can help reduce self-employment tax. S Corp owners are considered employees and must pay themselves a reasonable salary. The salary is subject to Social Security and Medicare taxes, but any additional profits distributed as dividends are not subject to self-employment tax.

Distribution of Profits:

LLCs offer flexibility in the distribution of profits. The profits can be distributed to owners in any way they choose, regardless of their ownership percentage. For example, if one owner owns 25% of the business, but the other owner did most of the work, the profits can be distributed accordingly.

S Corporations, on the other hand, must distribute profits based on the ownership percentage. This means that if one owner owns 25% of the business, they are entitled to 25% of the profits. S Corps are also limited to having only one class of stock, which means that all shareholders must have the same rights to distributions.

Legal Cases:

Perhaps if you get into a lawsuit as an LLC, you can lose your personal properties in the process whereas if your ecommerce is set up as an S Corp, your personal properties are most likely unaffected.

Conclusively LLCs are subject to self-employment tax on all profits and offer more flexibility in the distribution of profits. S Corps can help reduce self-employment tax by separating salary from dividends and must distribute profits based on the ownership percentage.

Ultimately, the best choice depends on the specific needs, goals of the business owners, and location of the business. For example whether you are an S Corp or not in NYC, the Unincorporated Business Tax may apply to you as well. States like Florida are known to be tax-friendly while California can be said to be tax-unfriendly.

#4 Excel is just fine, I need no ecommerce business software or accountant

Another mistake you must not make is to think you can take care of your bookkeeping without using a full accounting software. In most cases, many small business owners rely on Microsoft Excel which only keeps track of things and is subject to errors because it’s not an automatic entry.

The likes of Wave, FreshBooks, GoDaddy are not full accounting software and can’t be used for matching entries, confirming beginning and ending balance, reconciling and keeping track of the balance sheet, which tells you how much you have in assets, liabilities, owner’s equity and so on.

Such basic accounting software cannot cater for your growing business needs. Alternatively, QuickBooks is by far the most popular ecommerce accounting software in the US. It is efficient for every business size and just needs an accountant that understands your books to use it in the right way. You can also save time on bookkeeping and improve your margins using QB integration with PayTraQer.

In Australia, NewZealand and most European markets, Xero is more popular. Either way, you want to use a full functioning software to do your numbers right. If you keep giving a bunch of documents to your CPA so that you can file your taxes the next hour or day, you will only deprive yourself of the information needed to drive your business growth.

Outsourcing your bookkeeping to an accountant and doing it early in your business will help you take advantage of deductions, file taxes correctly and focus on growing your business.

#5 My business is not valuable because I don’t have enough cash at hand

Most ecommerce business owners mistake cash at hand for value or worth of their business. In inventory-based ecommerce, the faster or bigger you grow, the more inventory you deal with and the more cash you put out. E Commerce is cash hungry, you may make up to 100 million dollars and yet struggle to own cash.

A million dollars in revenue does not equate a big profit or cash at hand. The real value of your business is when you cash out by selling the business. What you are selling at that point is a brand; the great reviews, good reputation and the company’s potential to perform better in the future.

Without accurate bookkeeping done on an accrual basis, showing the trend and true condition of your business on a monthly basis over time, you cannot demonstrate its value to buyers.

For example, showing your buyer how your ecommerce business generated sales worth millions of dollars and over five hundred thousand dollars profit in the last six months on an accrual basis, the buyer can pay 3x or 4x your initial startup capital.

In essence, proper Etsy bookkeeping makes a sale look perfect so there are no holes for potential buyers and investors to pock and reduce the value you put out there for sale. In summary, the real value of your ecommerce business is the enterprise value not the monthly cash at hand.

#6 It’s stressful to track profit by SKUs

Another pitfall of online sellers is failure to track profit per SKUs. Sometimes it looks like your business is generally profitable whereas only the top SKUs are covering for the losses of other bottom SKUs.

Some SKUs might not get to the break even point not to say make profit. Only a SKU by SKU analysis of the holding cost and advert expense might reveal a need to update the price or reduce the number of SKUs.

#7 Nothing is at stake when I round off numbers on my books

In the context of financial reporting, rounding errors can have different implications depending on the accounting standards and the jurisdiction in which they are applied. This is particularly relevant when dealing with large volumes of transactions, such as those processed by banks.

Using the US Generally Accepted Accounting Principles (GAAP) as an example, let's consider a scenario where a bank processes 17,000 transactions worth a total of $100,000. Due to rounding errors, 250 of these transactions were recorded incorrectly, resulting in a discrepancy of $80. While this amount may seem negligible, it could still have an impact on financial reporting.

Under US GAAP, rounding errors of this nature are considered immaterial and can be expensed without further investigation. However, the situation could be different under International Financial Reporting Standards (IFRS), which require companies to assess materiality based on quantitative and qualitative factors.

If the same scenario occurred under IFRS, the ecommerce business would need to determine whether the rounding error is material enough to affect the financial statements. If so, it would need to correct the error and restate the financial statements accordingly.

In some countries, such as those that follow the Organization for Economic Cooperation and Development's (OECD) Common Reporting Standard (CRS), even small discrepancies can have serious consequences. For example, if the 238 rounding errors were related to foreign transactions, they could trigger an automatic exchange of information with the relevant tax authorities, potentially leading to penalties or fines.

Conclusion

Bookkeeping is a critical aspect of running a successful eCommerce business. Keeping accurate records of financial transactions can help you make informed decisions, comply with tax laws, and secure financing for growth. However, without proper bookkeeping practices, you can make errors and incur hidden costs that can harm your business's bottom line.

To avoid these mistakes and hidden costs, eCommerce businesses should establish proper bookkeeping procedures, invest in accounting software, and consider outsourcing to professional bookkeepers or accountants. By doing so, you can ensure that your financial records are accurate, up-to-date, and compliant with tax laws, allowing you to focus on growing your eCommerce business.

FAQs

What is the importance of bookkeeping for ecommerce businesses?

When properly done, ecommerce bookkeeping help your business in the following ways:

Provides insight into business performance

Facilitates better decision making

Supports growth and expansion

Enables accurate inventory management

Helps manage cash flow effectively

Provides clarity on financial status for investors and lenders

Helps with budgeting and forecasting

Enables comparison with industry benchmarks and competitors

Facilitates audit and due diligence requirements.

Helps with tax compliance

Which course is best for e-commerce?

The best course for an eCommerce business owner to take to gain a basic understanding of their business is E-Commerce Essentials. This course covers the basics of setting up an online store, optimizing it for search engines, managing inventory, fulfilling orders, and handling customer service.

What does an ecommerce bookkeeper do?

An eCommerce bookkeeper is responsible for managing the financial records of an online business, including recording transactions, reconciling accounts, preparing financial statements, and ensuring compliance with tax laws. They help eCommerce businesses make informed financial decisions and keep their finances organized and accurate.

How to do bookkeeping for an ecommerce business?

To do bookkeeping for an eCommerce business, one should set up a chart of accounts, record all transactions, reconcile accounts, prepare financial statements, track inventory and expenses, and ensure compliance with tax laws. It is recommended to use accounting software and seek professional help for complex financial matters.

What is accounting in e-commerce?

Accounting in eCommerce involves recording, classifying, and summarizing financial transactions of an online business. It includes tracking revenue, expenses, assets, liabilities, and equity, preparing financial statements, and ensuring compliance with tax laws. Effective accounting helps eCommerce businesses make informed financial decisions and achieve their financial goals.

What are the 4 areas of accounting practice?

The four areas of accounting practice are financial accounting, management accounting, auditing, and taxation. Financial accounting focuses on financial reports for external stakeholders, management accounting helps in decision-making for internal stakeholders, auditing ensures compliance with accounting standards, and taxation deals with tax compliance and planning.

What are the four common bookkeeping practices?

The four common bookkeeping practices are: 1) Recording financial transactions, 2) Classifying transactions into categories, 3) Reconciling accounts to ensure accuracy, and 4) Preparing financial reports. These practices help businesses keep track of their finances and make informed financial decisions.

Bookkeeping app for e-commerce

A bookkeeping app for eCommerce is a software application designed to help online businesses manage their financial records. It typically includes features such as invoicing, expense tracking, inventory management, and financial reporting. Bookkeeping apps can simplify bookkeeping tasks and improve the accuracy and organization of financial records.

E-commerce Bookkeeping Amazon Seller

E-commerce bookkeeping for Amazon sellers involves managing financial records of Amazon sales, fees, refunds, and other transactions. It also includes reconciling accounts, preparing financial statements, and ensuring compliance with tax laws. Effective bookkeeping for Amazon sellers helps in managing cash flow, optimizing profitability, and avoiding tax penalties.