Accounting for Retail Business - Retail Inventory Basics

Accounting is a pivotal aspect of managing retail businesses, focusing on precise tracking of finances and a keen eye on inventory costs. Retail accounting is a streamlined approach, particularly beneficial for store owners who must monitor their products closely.

This blog will explore retail accounting, its advantages and disadvantages, and whether it suits your business.

Contents

What is Retail Accounting?

Ways To Calculate The Cost Of Your Inventory

Retail Method of Accounting:

Example of Retail Accounting

Advantages and Disadvantages of Retail Accounting

Is the Retail Accounting Method Right For Your Business?

Streamline Your Financial Management with Advanced Accounting Solutions

FAQs

What is Retail Accounting?

Retail accounting simplifies the process of monitoring inventory costs compared to other methods. It uses retail accounting software to thoroughly track inventory at retail prices, helping identify stock losses, damages, and theft. This approach allows business owners to monitor the cost of sales, i.e., Cost of Goods Sold (COGS), also known as the retail inventory accounting method.

Additionally, the retail accounting method assists in managing the inventory you purchase or sell, ensuring you keep an eye on the remaining stock and helping maintain optimal inventory levels at all times. Given the sensitive financial and inventory data involved, it’s essential that accounting software includes strong security measures, according to Natallia Babrovich, Financial and Banking IT Consultant at ScienceSoft.

Ways To Calculate The Cost Of Your Inventory

Inventory plays a vital role in retail accounting, so selecting an appropriate inventory costing technique is crucial for your business and the products you offer. There are three methods for monitoring your inventory and assessing inventory costs:

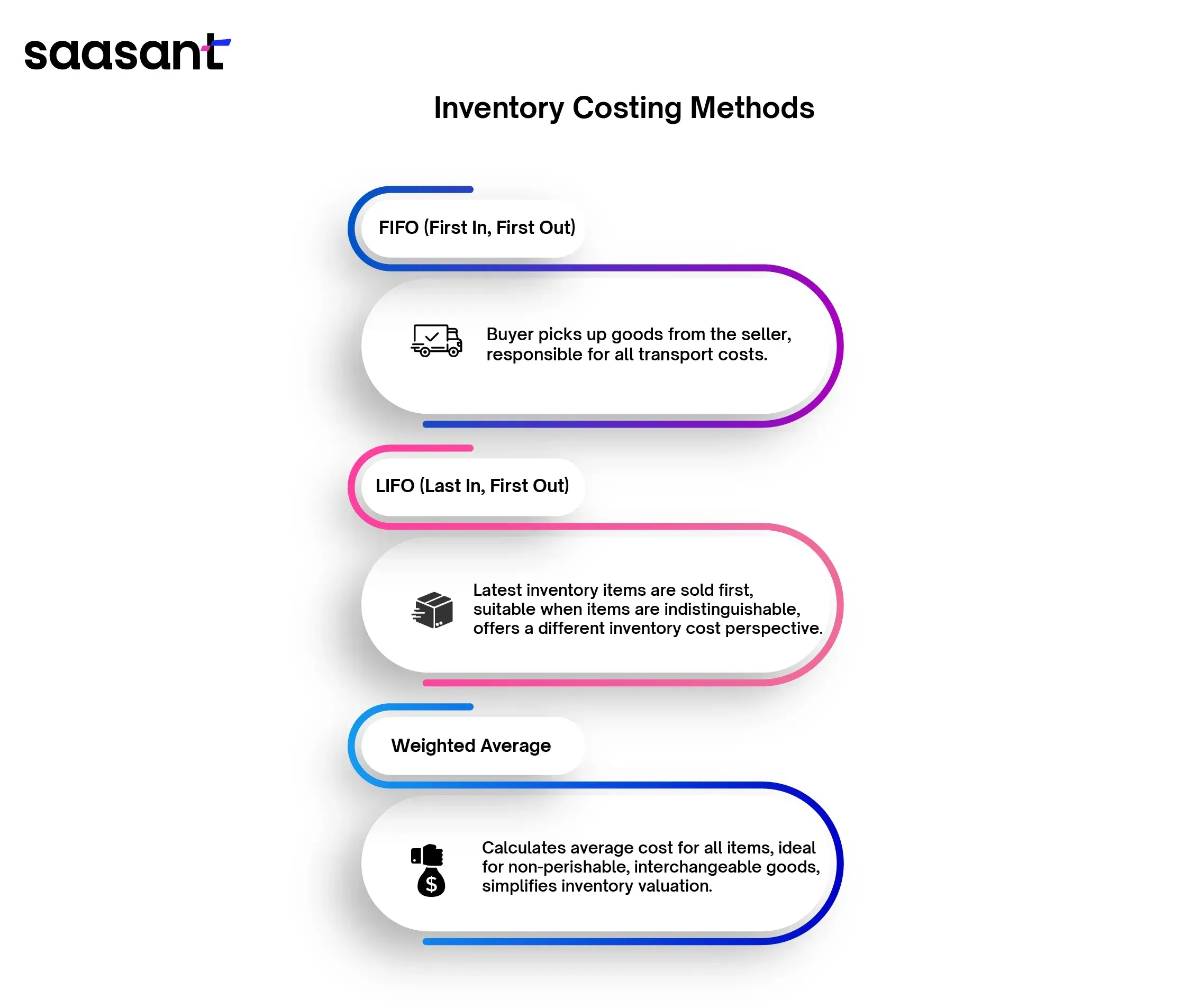

First In, First Out (FIFO)

Last In, First Out (LIFO)

Weighted Average

Each costing method offers unique advantages tailored to different types of inventory and business needs. Let's delve into each technique and understand the benefits it provides.

First In, First Out (FIFO Accounting):

FIFO accounting is relatively straightforward and a fundamental aspect of retail accounting. The FIFO method operates on the principle that the first items added to your inventory are also sold. This approach is particularly relevant for perishable goods, making it a popular choice among food retailers for its practical application.

FIFO accounting also posits that the valuation of remaining inventory at the end of an accounting period should reflect the most recent purchase prices. It is crucial to prevent spoilage or expired products, which would inevitably lead to disposal.

For instance, using the FIFO method to calculate inventory costs:

If 50 items are initially bought at $5 each and subsequently an additional 50 items are acquired (or manufactured) at a total cost of $7.5 each, FIFO would price the first item sold at $5. Once 50 items have been sold, the cost per item would be $7.5, based on the assumption that the oldest stock is sold initially.

Last In, First Out (LIFO Accounting):

It is another crucial accounting method for retail businesses of all sizes, distinct from FIFO primarily in its approach. LIFO accounting does the opposite of FIFO by assuming that the most recently added items to the inventory are sold first, as indicated by its name.

The LIFO method is beneficial when individual inventory units are indistinguishable from one another or when there's no practice of rotating stock to ensure older items are sold first. It's an essential retail accounting strategy for organizations looking to build their business from the ground up, providing a different perspective on inventory management and cost assessment.

With the same scenario:

If the first 50 items were bought at $5 each and another 50 items were later bought at $7.5 each, the LIFO method would assign a cost of $7.5 to the first items sold.

Weighted Average Method

The weighted average approach to valuing inventory is commonly applied when the goods are non-perishable and can be readily mixed or rotated.

Consider a container filled with rubber balls. Some balls were bought for $0.10 each, while others cost $0.12 each. Identifying the purchase price of each ball is impractical; therefore, the retailer calculates a weighted average cost and applies this average cost across the entire stock.

Retail Method of Accounting:

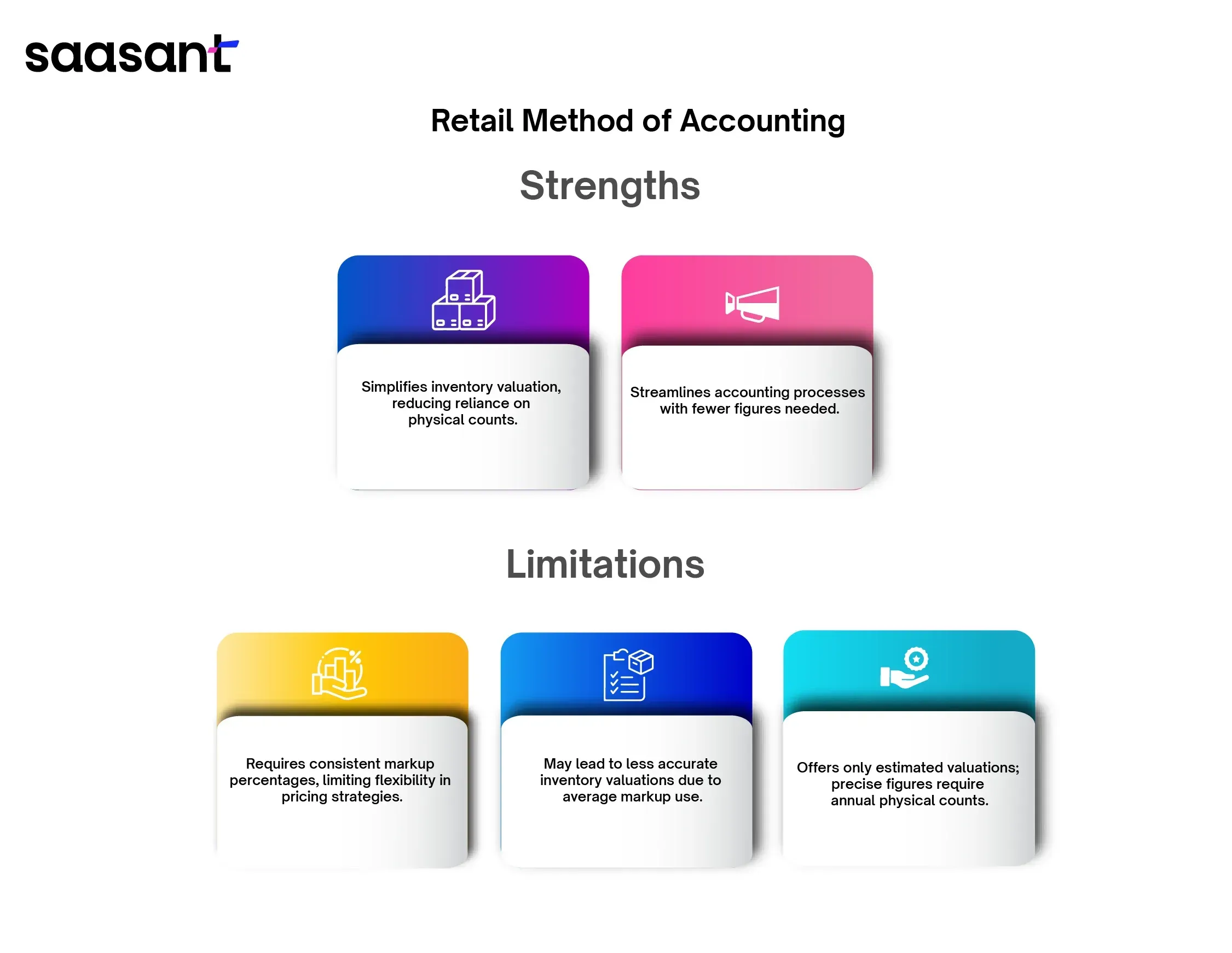

The retail method of accounting is one of the significant methods. It allows retailers to bypass physical inventory counts and ascertain inventory value, potentially enhancing retail business accounting over time.

However, the retail method has limitations: it is only effective when markup percentages are uniform across all inventory items. Variability in markup percentages across different items makes this method incapable of providing an accurate inventory valuation.

Having recognized the strengths and weaknesses of this accounting method, let's briefly review them.

The retail method simplifies calculations, allowing inventory cost to be determined with just a few figures and eliminating the need for a physical inventory.

Requires uniform markup across all items, which may not align with the varied pricing strategies employed by some retailers.

The use of average markup can reduce the accuracy of inventory valuations.

Provides only an estimated valuation; an annual physical inventory count is necessary for precise valuation.

Post-sale periods pose a challenge, as relying solely on the markup percentage needs to reflect inventory value in the current period accurately.

Example of Retail Accounting

Imagine your retail business selling various types of yarn and knitting accessories, with each fiber type and knitting needle set priced differently. Nevertheless, you have a 50% markup on all items, regardless of what they are.

Consider that you conducted a physical count of your inventory at the quarter's start, determining its initial cost value to be $80,000. Upon reviewing your sales data from the point-of-sale system, you note that your sales amounted to $30,000 by the quarter's end. Additionally, you invested $10,000 in restocking yarn and accessories during the quarter.

Using these figures, you can calculate the closing inventory value with the retail method as follows:

Starting Inventory (cost basis): $80,000

Additional Inventory Acquired (cost basis): $10,000

Total Inventory Available for Sale (cost basis): $90,000

Quarterly Sales (retail price): $30,000

Subtracting – Sales Cost: ($30,000 * 50%) = $15,000

Remaining Inventory Value (cost basis) – Sales Cost = Final Inventory Value

$90,000 – $15,000 = $75,000

Hence, it's reasonable to conclude that your inventory is valued at $75,000 at the quarter's close.

Advantages and Disadvantages of Retail Accounting

Let’s look into the advantages of retail accounting;

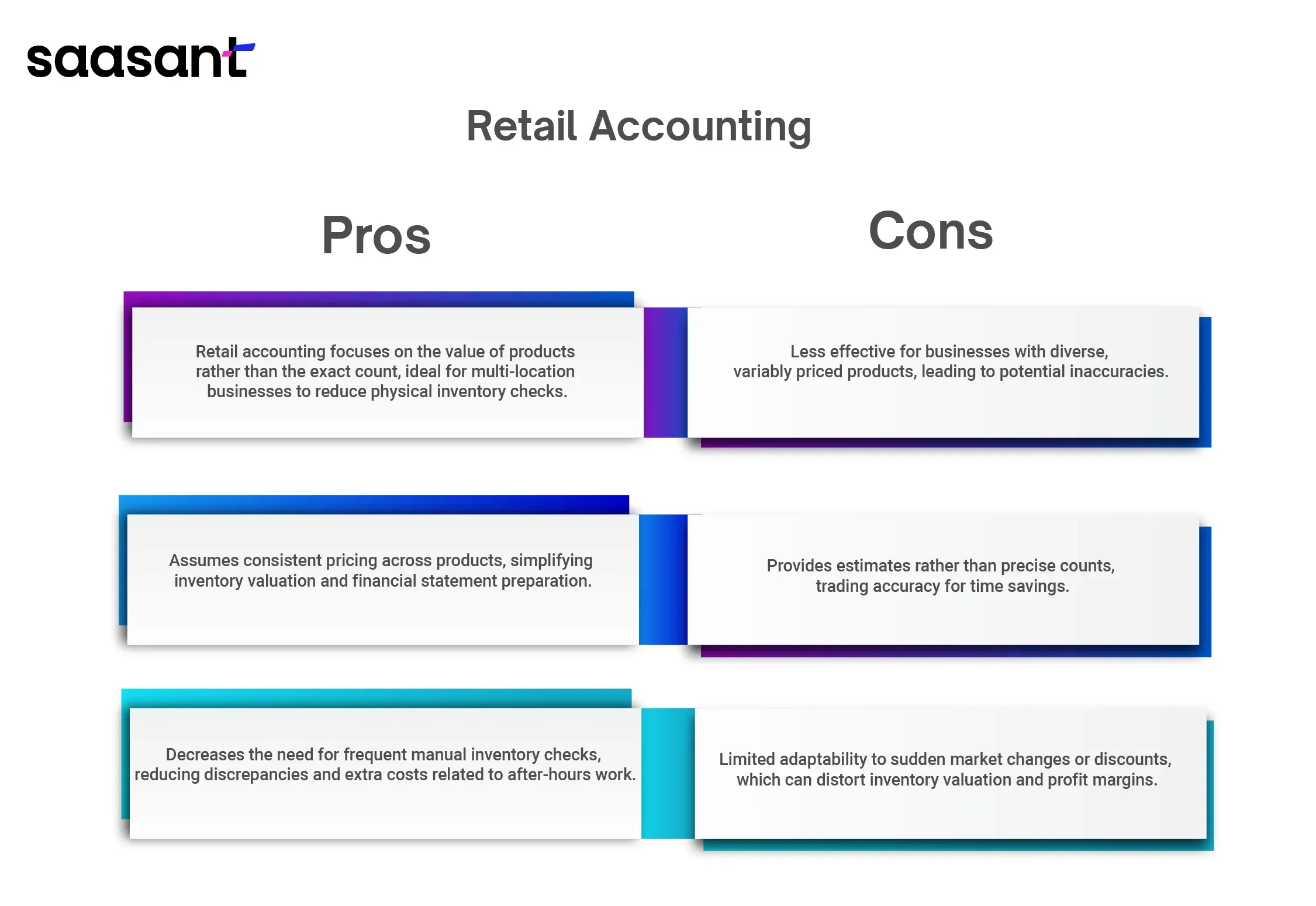

Ease of Use: Retail accounting prioritizes understanding product retail prices over the physical count of inventory. It mainly benefits businesses with multiple locations, reducing the need for extensive physical inventory checks.

Simplified Calculations: The retail accounting method assumes uniform pricing and price changes across all product units, making inventory valuation straightforward. This type of calculation helps in the easier preparation of financial statements.

Cost Savings: While manual inventory checks are essential, their frequency can be reduced with retail accounting, leading to cost savings. Manual counts often cause discrepancies in closing the store or paying staff for after-hours work, which can be minimized.

Some of the retail accounting disadvantages include;

Retail accounting offers a straightforward approach to gauging inventory levels but has limitations. The effectiveness of this method can vary depending on the diversity and pricing of the items you sell. Retail accounting might yield inaccurate figures for businesses with a wide range of products priced differently.

Another disadvantage is that retail accounting needs more consistency and precision; it generally offers approximate figures rather than exact counts. While it might save time compared to manually tallying inventory, the trade-off is potentially less accurate data.

Is the Retail Accounting Method Right For Your Business?

The retail accounting method depends on your business. The complexity of bookkeeping can be challenging for companies engaged in multi-channel sales or managing multiple physical stores. Here, the advantage of retail accounting is that it reduces the need for frequent physical stocktakes and potentially cuts costs.

However, a notable drawback is the potential need for adaptability with the retail method.

The retail method might be a good fit for those prioritizing ease and straightforwardness in their accounting practices. Yet, it's essential to be aware of its shortcomings, especially its inability to accurately reflect price reductions, sales, or changes in markup.

Look at its advantages and disadvantages carefully to determine if the retail method aligns with your business needs.

Streamline Your Financial Management with Advanced Accounting Solutions

You must employ several accounting strategies mentioned in this blog as a retailer. Despite its limitations, the retail accounting method is easy and saves time.

Remember, your financial management practices must adapt as your business expands. You may deal with a larger inventory, increased sales transactions, and the financial intricacies of operating multiple store locations. That is when an automation application like SaasAnt PayTraQer plays a crucial role in fetching the sales, fees, and refunds from e-commerce platforms or payment gateways and syncing them in QuickBooks or Xero. SaasAnt PayTraQer is an accounting automation software designed to streamline your bookkeeping efforts and automate operations, ensuring your business operates more efficiently than before. Additionally, it allows you to oversee your financial management while dedicating more attention to your retail operations.

If you want to learn more about finding marginal cost, check out this guide how to find marginal cost.

To learn how to add inventory in QuickBooks, refer to this guide.

FAQs

What is the basis of accounting for retail?

The basis of accounting for retail involves recording financial transactions from sales of goods and services. Retailers can use cash-based accounting, where transactions are recorded only when cash is exchanged, or accrual-basis accounting, where transactions are recorded when they are earned or incurred, regardless of cash movement.

What is the retail method of accounting in SAP?

The retail method of accounting in SAP refers to a system used to manage inventory valuation and cost of goods sold in a retail setting. It estimates the ending inventory value by applying a cost-to-retail price ratio to the retail value of inventory. SAP's retail method simplifies inventory management and financial reporting by integrating sales, purchases, and inventory data.

How do you calculate the retail method?

To calculate the retail method, follow these steps:

Determine the total cost and retail price of goods available for sale.

Calculate the cost-to-retail ratio by dividing the total cost by the total retail price.

Find the ending inventory at retail price.

Apply the cost-to-retail ratio to the ending inventory at retail price to estimate the ending inventory at cost.