Account Reconciliation: The Basics of Reconciling Accounts

Account reconciliation serves as the financial compass for businesses, ensuring accuracy, fraud detection, compliance adherence, and optimal cash flow management. It's the cornerstone for informed decision-making and maintaining financial health. This practice fosters financial integrity and cultivates trust among stakeholders, reinforcing the reliability of business operations.

Contents

What is Account Reconciliation?

How to do Bank Reconciliation in QuickBooks Online?

Simplifying Bank Reconciliation Using SaasAnt Transactions

How do I Fix a Messed Up Reconciliation in QuickBooks Online?

Mistakes in Bank Reconciliation: Problems and Solutions

Bank Reconciliation Best Practices

Conclusion

Frequently Asked Questions

What is Account Reconciliation?

Account reconciliation is comparing financial records or accounts to ensure they are accurate and in agreement. It's like double-checking to ensure that the money going in and out of your accounts matches what should be there based on your transactions and other financial activities.

For example, if you have a bank account, you might reconcile it by comparing your bank statement (which shows all the transactions processed by the bank) with your records of deposits, withdrawals, checks written, and electronic transfers. The goal is to identify any discrepancies, such as missing transactions, errors in amounts, or unauthorized charges, and then make corrections as needed to ensure that your records accurately reflect your financial position.

Why is Account Reconciliation Important?

Accuracy: It ensures that your financial records are accurate and up to date, reflecting the actual financial position of your business. This accuracy is essential for making informed decisions and meeting regulatory requirements.

Fraud Detection: Reconciliation helps detect discrepancies and anomalies in financial transactions, which can indicate fraud or errors. Early detection through reconciliation can prevent economic losses and protect your business from fraud.

Financial Control: Reconciliation provides a control mechanism to monitor and manage your finances effectively. It helps identify errors, unauthorized transactions, or unusual activities, allowing you to take corrective actions promptly.

Compliance: Many regulatory bodies and accounting standards require regular reconciliation for financial reporting and compliance. These standards ensure transparency, accountability, and trustworthiness in your financial operations.

Cash Flow Management: Reconciliation helps track cash flow by comparing actual transactions with expected ones. It enables you to manage cash effectively, identify discrepancies early, and avoid cash flow disruptions.

Decision Making: Accurate and reconciled financial data provides a solid foundation for strategic business decisions. It helps you assess your business's economic health, identify trends, and plan for future growth and investments.

How to do Bank Reconciliation in QuickBooks Online?

Performing bank reconciliation in QuickBooks Online involves matching your bank and credit card statements with the transactions recorded in QuickBooks. Here are the steps to reconcile a bank account in QuickBooks Online:

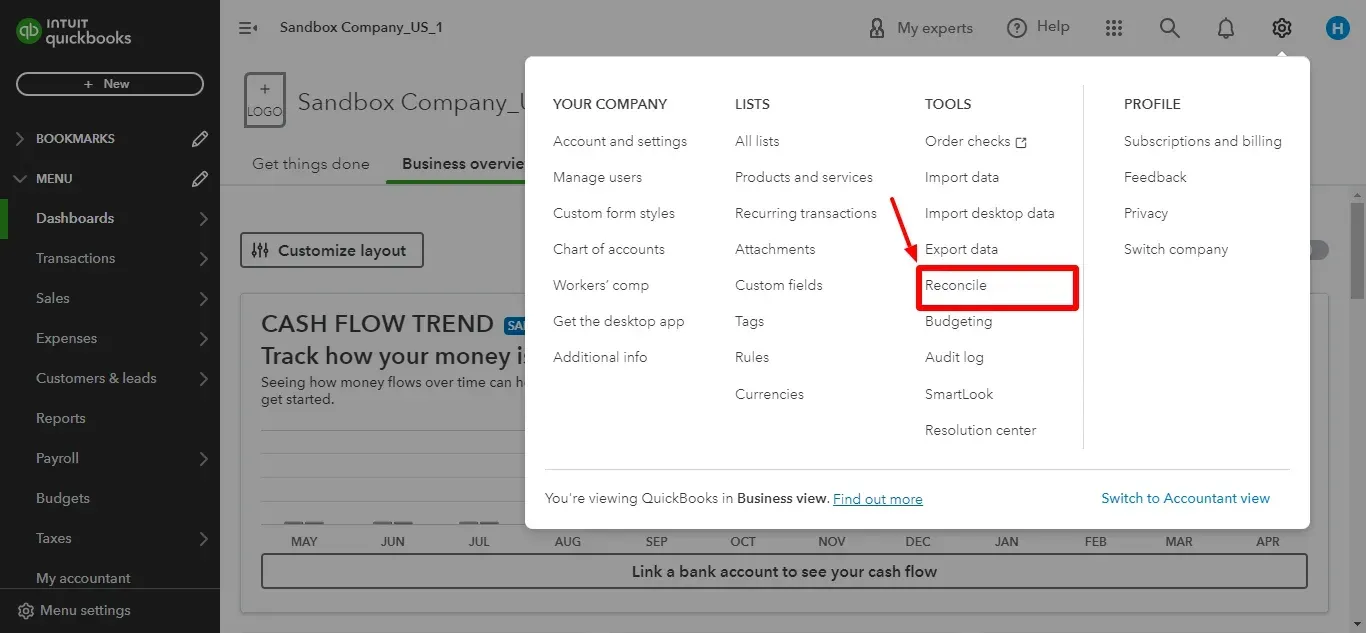

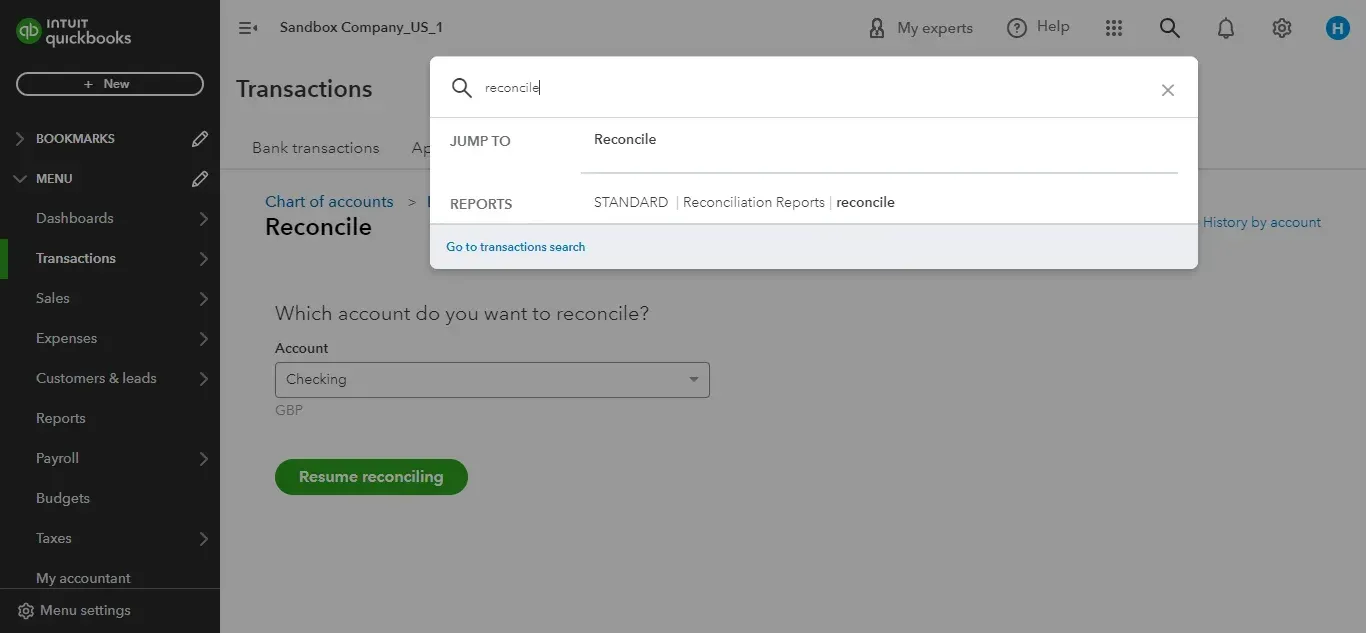

Access the Reconcile Menu:

Click on the Gear icon in the upper right corner and select "Reconcile" from the dropdown menu.

Alternatively, you can search for "Reconcile" using the search bar.

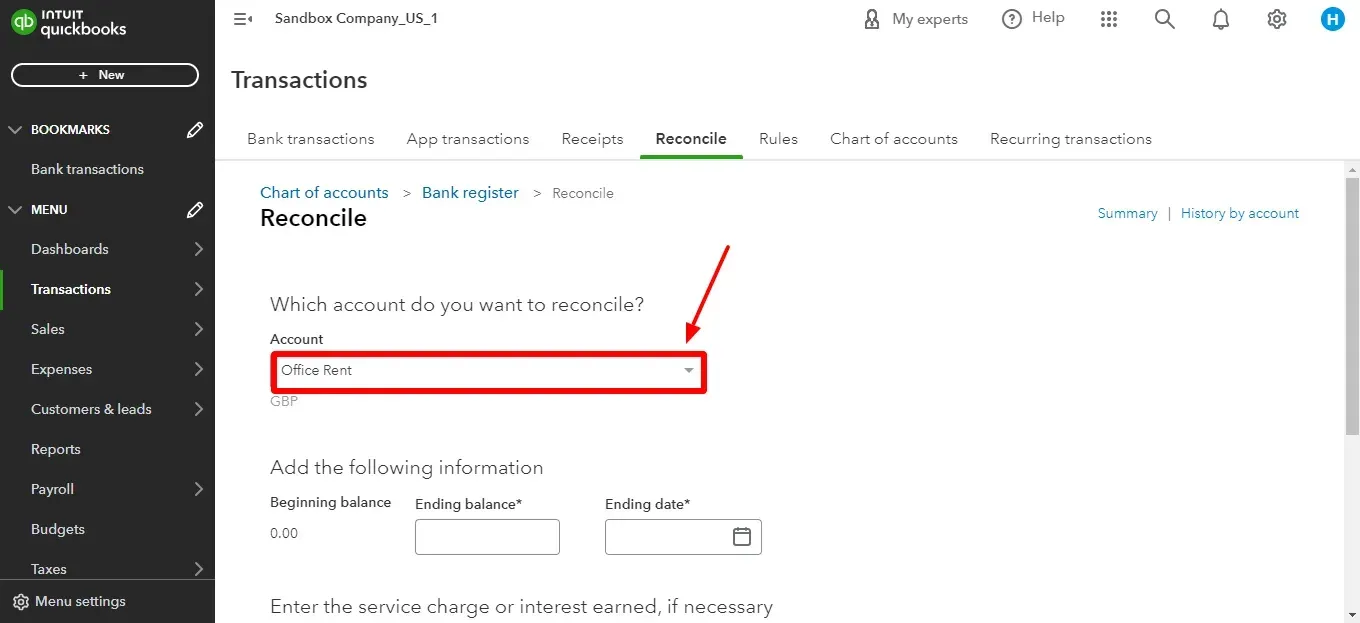

Select the Account:

From the "Account" dropdown menu, choose the specific bank account you want to reconcile.

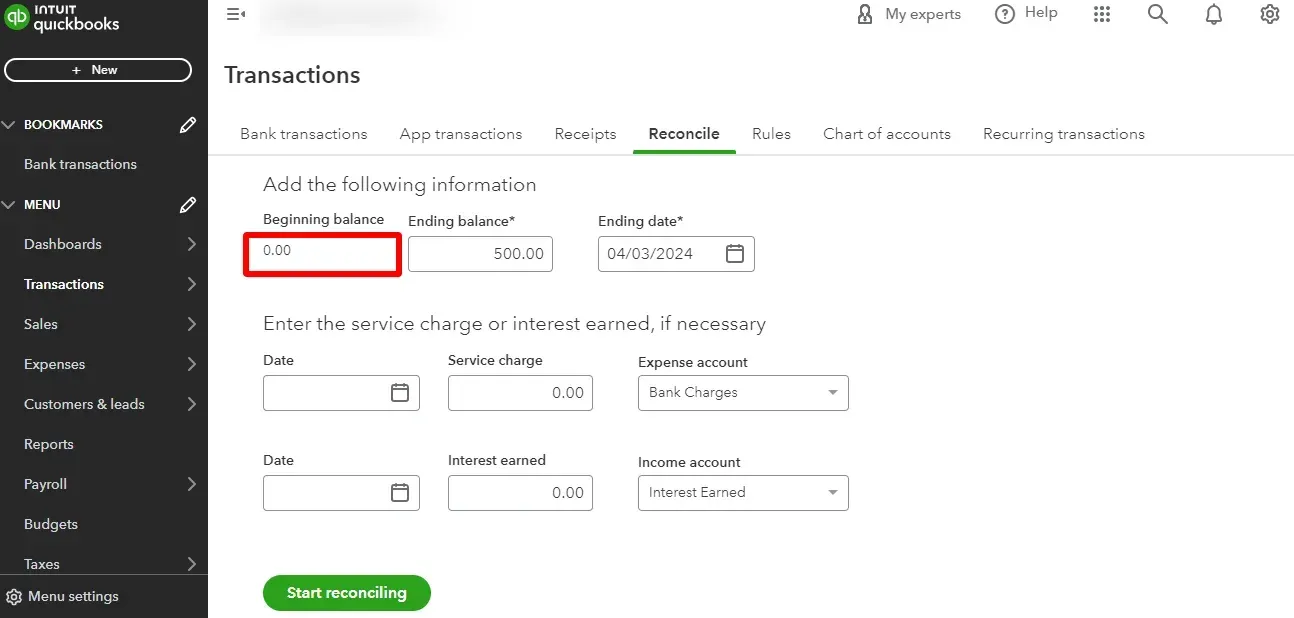

Review Opening Balance:

Verify that the "Beginning balance" in QuickBooks Online matches the opening balance on your bank statement. If there's a discrepancy, investigate or adjust it before proceeding.

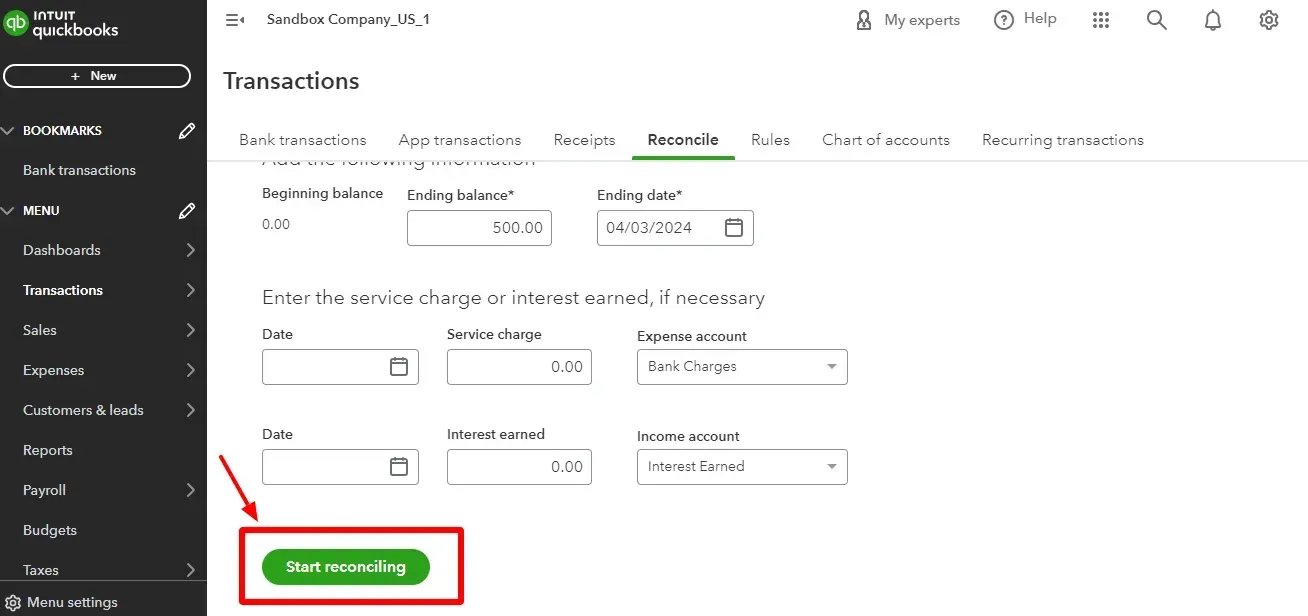

Start Reconciling:

Click on "Start reconciling" now.

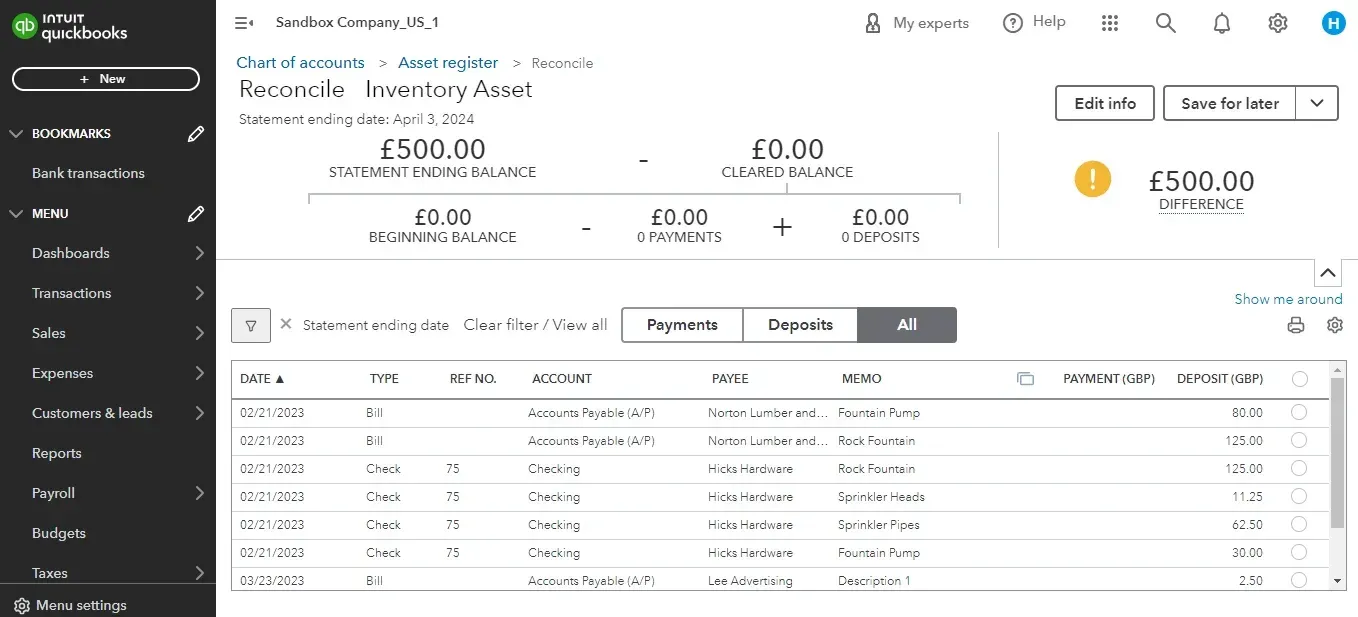

Match Transactions:

You'll have a list of transactions in QuickBooks Online. Minimize the downloaded file list of transactions from your bank statement and keep it visible on one side of the screen.

Carefully compare each transaction manually. If you find a matching transaction in your bank statement, click the checkbox next to the amount in QuickBooks Online. This marks it as reconciled.

Handle Discrepancies:

Transactions appearing in QuickBooks Online but not on your statement might require further investigation. You should categorize them differently, edit the amount, or mark them as uncleared for ongoing issues.

Transactions on your bank statement that aren't in QuickBooks Online might be deposits you still need to record or bank fees. You'll need to manually add these transactions to QuickBooks Online.

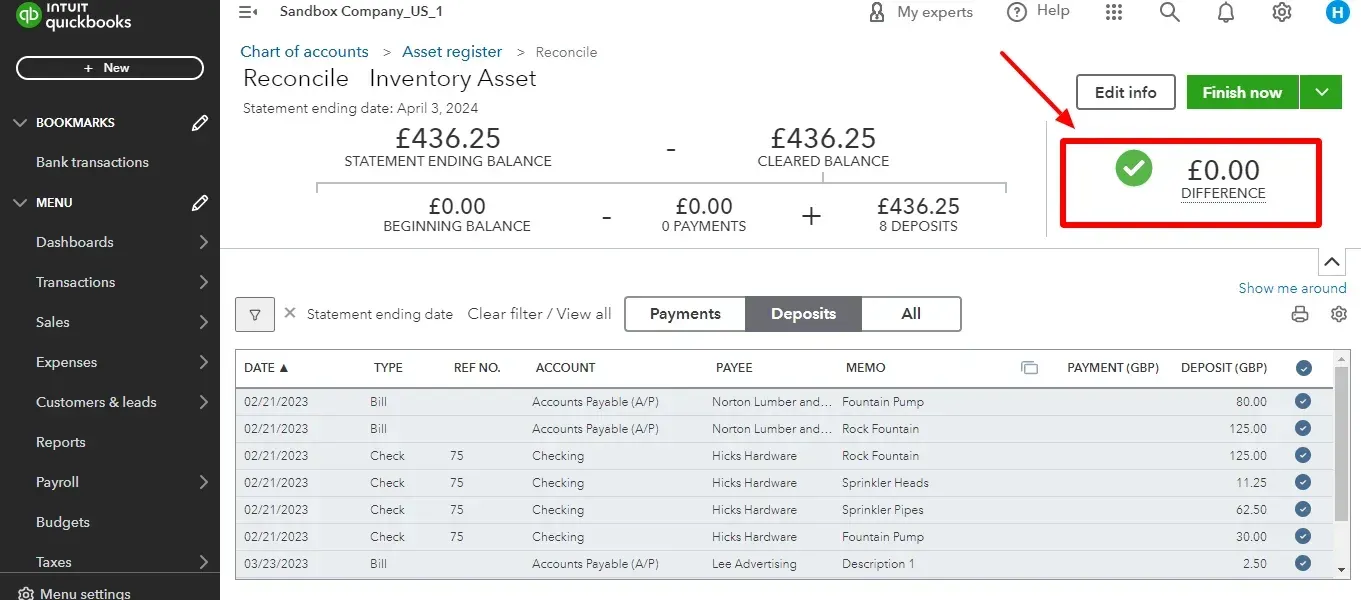

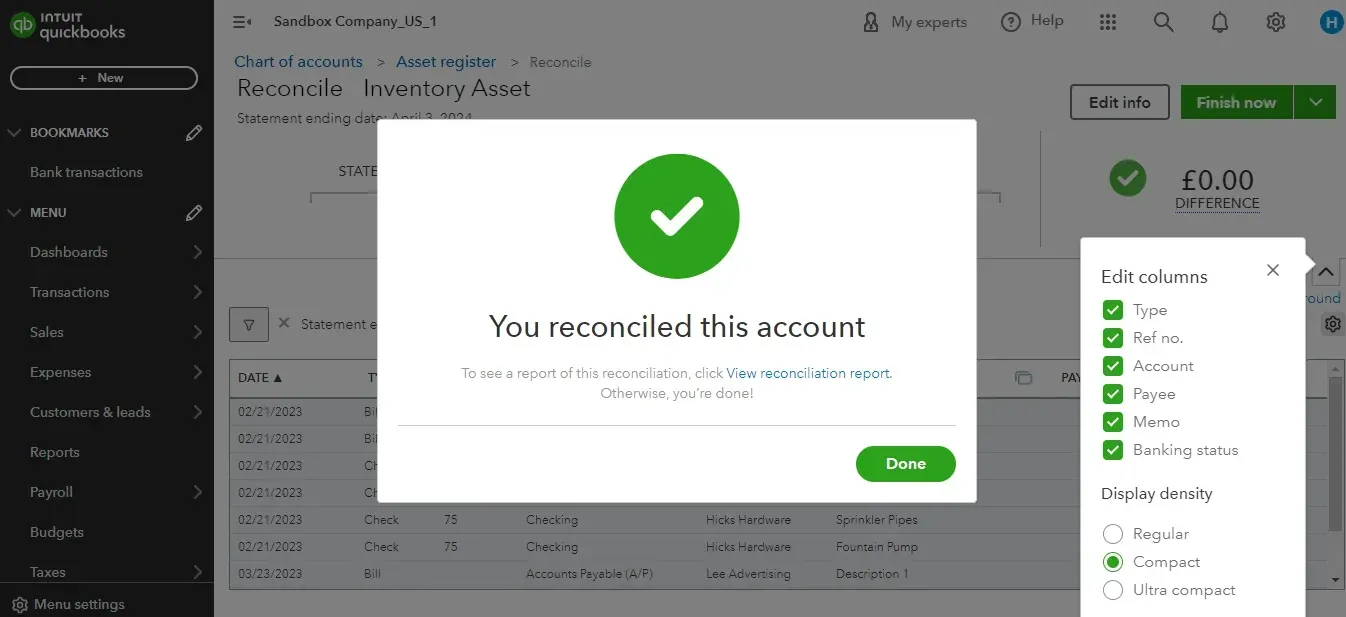

Finalize Reconciliation:

Once you've reviewed and matched (or addressed) all transactions, you should ideally have a difference of $0.00 between your reconciled balance in QuickBooks Online and the ending balance on your bank statement.

If there's a minor difference (a few cents due to rounding), you can accept it or investigate further.

When satisfied, click on "Finish now" to finalize the reconciliation.

Regular bank reconciliation in QuickBooks Online helps ensure your financial records are accurate and current, making tracking cash flow and financial performance easier.

Simplifying Bank Reconciliation Using SaasAnt Transactions

Bank reconciliation can be tedious, especially for businesses with high transaction volumes. But what if there was a way to simplify the process and save valuable time? SaasAnt Transactions seamlessly integrates with QuickBooks Online to transform your bank reconciliation experience.

Importing Bank Transactions into QuickBooks Through SaasAnt Transactions

Here are quick Instructions for importing bank transactions into QuickBooks Online

Log in to your QuickBooks Online account.

Navigate to the 'Apps' tab and find 'SaasAnt Transactions.'

Connect SaasAnt Transactions with your QuickBooks Online account.

Click 'New Import' to start the import process for bank transactions.

Upload your file (supports various formats, including Excel, CSV, and IIF).

Map the fields in your file correctly with QuickBooks fields in the mapping screen.

Review the mapping for accuracy and initiate the import.

Validate the imported data in QuickBooks Online to ensure accuracy.

Challenges of Manual Reconciliation:

Time-consuming: Manually entering and comparing transactions can be lengthy and error-prone.

Prone to Errors: Data entry mistakes, missed transactions, and categorization inconsistencies can lead to inaccurate records.

Inefficient: Manual reconciliation takes away time from other crucial financial tasks.

SaasAnt Transactions to the Rescue:

SaasAnt Transactions offers a powerful solution for automating and simplifying bank reconciliation in QuickBooks Online. Here's how it streamlines the process:

Effortless Import: You can import your bank statements (Excel, CSV, IIF) directly into SaasAnt Transactions. No more manual data entry!

Automated Matching: SaasAnt uses intelligent algorithms to match transactions between your bank statement and QuickBooks Online, saving you significant time and effort.

Duplicate Detection: SaasAnt's built-in duplicate detection feature eliminates the risk of duplicate entries, ensuring data accuracy.

Customization: Customize how transactions are mapped and categorized to match your QuickBooks Online setup perfectly.

Benefits of Using SaasAnt Transactions:

Increased Accuracy: Automated matching and duplicate detection minimize errors, leading to more reliable financial records.

Improved Efficiency: Free yourself from tedious manual work and focus on higher-value tasks.

Time Savings: Automate repetitive tasks and save significant time during reconciliation.

Simplified Compliance: Accurate and timely reconciliations help ensure compliance with tax regulations.

How SaasAnt Transactions Integrate with QuickBooks Online?

Connect SaasAnt Transactions: Locate the "Apps" section within QuickBooks Online and search for "SaasAnt Transactions." Once found, connect and integrate the app with your QuickBooks Online account.

Import Bank Statements: Upload your bank statement files (Excel, CSV, IIF) into SaasAnt Transactions.

Automatic Matching: SaasAnt will automatically match transactions between your uploaded statement and your QuickBooks Online data.

Review and Approve: Review the automatically matched transactions and make any necessary adjustments before finalizing the reconciliation in QuickBooks Online.

How do I Fix a Messed Up Reconciliation in QuickBooks Online?

Fixing a messed-up reconciliation in QuickBooks Online involves identifying and correcting the errors that caused the discrepancy. Here's a breakdown of the steps you can take:

1. Identify the Discrepancy:

Open the "Reconcile" menu (Gear icon -> Reconcile).

Select the previously reconciled account.

Look for the "Ending Balance" displayed in QuickBooks Online.

Compare it to the ending balance on your corresponding bank statement.

If there's a difference, this indicates a reconciliation error.

2. Review Unmatched Transactions:

In the "Reconcile" window, check for any transactions that haven't been marked as reconciled (unchecked boxes).

Unmatched transactions in QuickBooks Online could be:

Missing from your bank statement: These might be deposits yet to be recorded or outstanding checks. You'll need to add them manually in QuickBooks Online.

Miscategorized: Review the transaction details and ensure they are categorized correctly in QuickBooks Online.

Unmatched transactions on your bank statement could be:

Bank fees or service charges must be added as QuickBooks Online expense transactions.

Deposits still need to be recorded: If a deposit appears on your statement but not in QuickBooks Online, you'll need to add it manually.

3. Investigate Discrepancies:

For any unmatched or mismatched transactions, you might need to:

Review source documents: Check invoices, receipts, or bank statements for reference.

Consult with colleagues: If the discrepancy involves another department (e.g., sales or accounts payable), discuss it with them to understand the transaction details.

4. Correct the Errors:

Once you understand the cause of the discrepancy, you can take corrective actions:

Edit transactions: If a transaction amount is incorrect in QuickBooks Online, edit it to match the bank statement.

Categorise transactions: Ensure transactions are categorized appropriately in QuickBooks Online.

Add missing transactions: Add any missing deposits, bank fees, or outstanding checks to QuickBooks Online.

5. Undo Reconciliation:

In some cases, a complete redo might be necessary. QuickBooks Online allows you to undo the last reconciliation for a specific account.

Caution: This should only be done as a last resort, as it will remove all previously marked reconciliations. Make sure you have a backup of your data before proceeding.

Mistakes in Bank Reconciliation: Problems and Solutions

Mistakes in bank reconciliation can lead to inaccuracies in financial reporting and decision-making. Here are common errors to watch for and how to avoid them:

Transaction Omissions:

Problem: Forgetting to record transactions in QuickBooks or on the bank statement.

Solution: Regularly review and compare both QuickBooks entries and bank statements to ensure all transactions are recorded.

Timing Differences:

Problem: Some transactions may not appear on the bank statement if they haven’t cleared the bank by the statement's end date.

Solution: Understand the timing of transactions and ensure they are recorded in the correct period. Regularly follow up on outstanding checks or deposits.

Data Entry Errors:

Problem: Mistyping the transaction amount or recording it in the wrong account.

Solution: Double-check entries for accuracy and correct account allocation. Utilise QuickBooks’ import features to minimize manual data entry.

Duplicate Transactions:

Problem: Recording the same transaction more than once in QuickBooks.

Solution: Regularly review the account register for duplicate entries and remove any redundancies.

Incorrect Opening Balance:

Problem: Starting a reconciliation with an incorrect opening balance, often due to errors in previous reconciliations.

Solution: Ensure the ending balance of the previous reconciliation matches the opening balance of the current period. Resolve any past discrepancies before proceeding.

Failure to Reconcile Regularly:

Problem: Infrequent reconciliation can lead to a buildup of errors and make them more challenging to resolve.

Solution: Reconcile your accounts monthly to catch and correct errors promptly.

Not Reviewing for Unauthorized Transactions:

Problem: Missing fraudulent or unauthorized transactions.

Solution: Carefully review each transaction during reconciliation to identify any unauthorized or suspicious activity.

Bank Reconciliation Best Practices

Bank reconciliation ensures your financial records match your bank statements, preventing errors and keeping your finances organized. Here are some best practices to streamline the process:

Establish a Risk-Based Approach:

Not all accounts require the same level of scrutiny. Identify high-risk accounts with frequent transactions or a higher likelihood of errors for more frequent reconciliation.

Standardize the Process:

Create a clear and consistent workflow for all reconciliations. This includes defining roles, deadlines, and documentation procedures. Standardizing the process minimizes confusion and ensures everyone's on the same page.

Automate When Possible:

Leverage technology! Many accounting software solutions, like QuickBooks Online, offer automated bank reconciliation features. These can automate data entry matching and even identify potential discrepancies.

Reconcile Regularly:

The frequency of reconciliation depends on your transaction volume and risk tolerance. Weekly or bi-weekly reconciliations are common, but daily might be necessary for high-risk accounts.

Document Everything:

Maintain a record of your reconciliation process, including reconciliation reports and any adjustments made. This helps with future audits and ensures a clear history of your financial activities.

Segregate Duties:

Implement internal controls by separating the tasks of recording transactions, reconciling accounts, and handling bank statements. This minimizes the risk of errors and fraud.

Review Discrepancies Promptly:

Don't leave unmatched transactions lingering. Investigate discrepancies as soon as they arise to promptly identify and address any underlying issues.

Perform Reviews Regularly:

Evaluate your reconciliation process periodically. Look for areas for improvement, such as automating more tasks or adjusting the frequency of reconciliation for specific accounts.

Conclusion

Account reconciliation is an essential financial activity that ensures the accuracy and reliability of a business's financial records. By comparing internal records with external bank statements, companies can verify the correctness of their financial transactions, detect fraud, maintain regulatory compliance, manage cash flow effectively, and support strategic decision-making.�

Employing best practices such as regular reconciliation, standardizing processes, using automation, and maintaining thorough documentation can significantly enhance the efficiency and accuracy of reconciliation processes. SaasAnt Transactions offers a practical solution to streamline and improve the reconciliation process in QuickBooks Online, saving time and reducing errors. Practical account reconciliation solidifies a business's financial foundation, fostering stakeholder trust and supporting sustained growth and economic health.

Frequently Asked Questions

What exactly is account reconciliation, and why is it necessary?

Account reconciliation is verifying that the financial transactions in a company's accounting records match the corresponding bank statements. It is necessary to ensure financial accuracy, detect potential fraud, adhere to compliance standards, manage cash flow efficiently, and facilitate informed decision-making.

How often should account reconciliation be performed?

The frequency of account reconciliation depends on the volume of transactions and the business's specific needs. While monthly reconciliation is common and generally recommended, companies with high transaction volumes or those in regulated industries might need to reconcile their accounts more frequently, such as weekly or daily.

Can account reconciliation help in detecting fraud? How?

Yes, account reconciliation can play a critical role in detecting fraud. Disc discrepancies can be identified by systematically comparing the company’s records with bank statements that may indicate fraudulent activity, such as unauthorized transactions, altered checks, or embezzlement. Regular reconciliation helps in the early detection and mitigation of financial losses.

What are the challenges of manual reconciliation?

Manual reconciliation can be time-consuming, error-prone, and inefficient. Challenges include data entry mistakes, missed transactions, and difficulty tracking discrepancies. Software like SaasAnt Transactions addresses these issues by automating the import and matching of bank transactions with QuickBooks Online, reducing manual entry, improving accuracy, and saving time.

What steps should be taken if discrepancies are found during the reconciliation process?

If discrepancies are found, the first step is carefully reviewing and comparing the transactions in question against bank statements and source documents. It's essential to identify whether the discrepancy is due to a recording error, an omitted transaction, or an unauthorized transaction. Once identified, appropriate adjustments should be made in the accounting records, such as editing incorrect entries, adding missing transactions, or investigating potential fraudulent activities.

How can reconciliation be done quickly in QuickBooks Online?

To easily do reconciliation in QuickBooks Online, you can use Saasant Transactions, which seamlessly integrates with QuickBooks Online to simplify and automate the bank reconciliation process. Here's how you can utilize Saasant Transactions for efficient reconciliation:

Import Bank Transactions: Log in to your QuickBooks Online account, navigate to the 'Apps' tab, and find 'Saasant Transactions.' Connect Saasant Transactions with your QuickBooks Online account. Click 'New Import' to start importing bank transactions.

Upload Your File: Saasant Transactions supports various file formats like Excel, CSV, and IIF. Upload your bank statement file into Saasant Transactions.

Map Fields and Review: The fields in your file are correctly mapped with QuickBooks fields in the mapping screen. Review the mapping for accuracy and initiate the import.

Validate Imported Data: Once the import is complete, validate the imported data in QuickBooks Online to ensure accuracy.